Low Housing Supply Squeezes Affordability

Rental affordability is as bad as it's ever been across the U.S., in part because there are not enough new, affordable units to meet demand

- U.S. renters can expect to spend 30.1 percent of their income on rent, while homebuyers can expect to spend about 15.3 percent of their monthly income on a mortgage payment.

- Affordability is worst in fast-growing cities that have fallen behind in building homes to keep up with population growth.

- The U.S. Zillow Rent Index was up 3.4 percent year-over-year in February to $1,355. The Zillow Home Value Index rose 4.9 percent year-over-year to $178,700.

SEATTLE, March 27, 2015 /PRNewswire/ -- The least affordable housing markets are those where new housing permits have not kept up with population growth, according to a Zillow® analysis of U.S. rental and mortgage affordabilityi.

Affordability is best in places that either have slow population growth – such as Detroit – or have met new growth by building new housing units. Chicago, for example, permitted 906 new housing units in 2012 and 2013 for every 1,000 new residents between 2013 and 2014ii. Chicago renters can expect to spend about 31% of their income on rent, while homebuyers there can expect to put 13.9% of their income toward house payments.

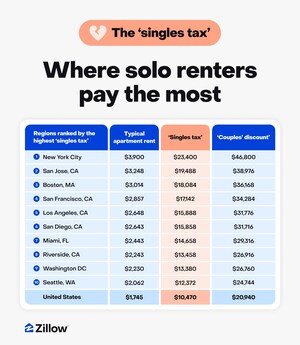

It's easy to see how San Francisco has become one of the country's least affordable housing markets: Zillow's analysis showed that for every 1,000 new residents, there were just 193 new housing units permitted. Residents of the San Francisco metro can expect to spend 44 percent of their income on rent, or 39.2 percent on a monthly mortgage payment.

The short supply is no secret to policy-makers. The mayor of San Francisco has pledged to add 30,000 housing units by 2020iii, and a Boston city report made a similar recommendation to meet demand with 53,000 new housing units by 2030iv.

"As the economy continues to improve, more Americans are slowly moving off of their buddies' couches and out of their parents' basements into homes of their own, first likely as renters and then eventually as homebuyers," said Zillow Chief Economist Dr. Stan Humphries. "Unfortunately, the supply of affordable homes, especially affordable rentals, is insufficient in many areas to meet this growing demand. As a result, the competition for those homes that are available can often be fierce, driving up prices and contributing to worsening affordability. More construction will help ease the crunch, and getting a mortgage is also getting easier, which will help more current renters transition to homeownership and further ease rental inventory shortages. But these fixes won't happen overnight."

Since 2000, rents have grown at roughly twice the pace of incomes. Partially as a result, the percentage of Americans citing "cheaper housing" as a reason they moved to a different home has almost doubled since then, from 5.6 percent to 9.6 percent currently, according to the U.S. Census Bureauv.

Over the past several years, renting – historically a budget-minded choice – has become increasingly less affordable. Meanwhile, recovering home prices, along with historically low mortgage rates, have made buying more affordable than it was historically, on a monthly basisvi. Zillow's February Real Estate Market Reports showed home values up 4.9 percent year-over-year to a Zillow Home Value Index of $178,700. U.S. rents rose 3.4 percent to a Zillow Rent Index of $1,355.

| Metro area |

February ZHVI |

Percentage of Monthly Income Spent on Mortgage Payment (2014 Q4) |

Percentage of Monthly Income Spent on Rent (2014 Q4) |

Permits per 1000 new residents |

| United States |

$178,700 |

15.3% |

30.1% |

384 |

| New York- Northern New Jersey |

$383,300 |

26.2% |

41.6% |

383 |

| Los Angeles, CA |

$533,700 |

40.1% |

48.2% |

187 |

| Chicago, IL |

$187,100 |

13.9% |

31.1% |

906 |

| Dallas-Fort Worth, TX |

$155,700 |

11.6% |

28.5% |

312 |

| Philadelphia, PA |

$202,800 |

15.2% |

30.0% |

671 |

| Houston, TX |

N/A |

11.9% |

30.3% |

376 |

| Washington, DC |

$362,800 |

17.9% |

27.0% |

332 |

| Miami-Fort Lauderdale, FL |

$212,500 |

20.2% |

44.2% |

223 |

| Atlanta, GA |

$154,900 |

12.3% |

25.4% |

301 |

| Boston, MA |

$369,100 |

22.4% |

33.8% |

299 |

| San Francisco, CA |

$715,800 |

39.2% |

44.0% |

193 |

| Detroit, MI |

$114,400 |

10.0% |

24.6% |

1,813 |

| Riverside, CA |

$285,200 |

23.8% |

36.4% |

167 |

| Phoenix, AZ |

$203,400 |

17.4% |

28.0% |

250 |

| Seattle, WA |

$343,900 |

21.9% |

30.8% |

353 |

| Minneapolis-St Paul, MN |

$211,400 |

14.2% |

25.9% |

380 |

| San Diego, CA |

$474,100 |

34.0% |

43.2% |

188 |

| St. Louis, MO |

$132,500 |

10.8% |

24.4% |

1,036 |

| Tampa, FL |

$148,600 |

14.4% |

32.1% |

314 |

| Baltimore, MD |

$244,100 |

15.9% |

29.2% |

400 |

| Denver, CO |

$289,200 |

19.8% |

33.4% |

305 |

| Pittsburgh, PA |

$125,300 |

10.8% |

25.2% |

42,258 |

| Portland, OR |

$281,400 |

20.9% |

30.9% |

376 |

| Sacramento, CA |

$335,700 |

26.0% |

33.2% |

159 |

| San Antonio, TX |

N/A |

12.4% |

29.0% |

166 |

| Orlando, FL |

$170,100 |

16.3% |

32.7% |

339 |

| Cincinnati, OH |

$138,000 |

11.4% |

25.8% |

554 |

| Cleveland, OH |

$119,700 |

10.9% |

27.4% |

1,311 |

| Kansas City, MO |

N/A |

10.9% |

24.9% |

517 |

| Las Vegas, NV |

$187,600 |

16.1% |

27.1% |

242 |

| San Jose, CA |

$852,800 |

39.5% |

39.4% |

294 |

| Columbus, OH |

$146,300 |

11.6% |

26.2% |

528 |

| Charlotte, NC |

$158,900 |

13.2% |

26.8% |

472 |

| Indianapolis, IN |

$129,100 |

10.8% |

26.3% |

390 |

| Austin, TX |

N/A |

15.9% |

31.0% |

486 |

| Virginia Beach, VA |

$211,300 |

15.1% |

26.7% |

588 |

About Zillow Research

Zillow® is the leading real estate and rental marketplace dedicated to empowering consumers with data, inspiration and knowledge around the place they call home, and connecting them with the best local professionals who can help. In addition, Zillow operates an industry-leading economics and analytics bureau led by Zillow's Chief Economist Dr. Stan Humphries. In 2015, Dr. Humphries co-wrote and published the New York Times' bestselling "Zillow Talk: The New Rules of Real Estate." Dr. Humphries and his team of economists and data analysts produce extensive housing data and research covering more than 450 markets at Zillow Real Estate Research. Zillow also sponsors the quarterly Zillow Home Price Expectations Survey, which asks more than 100 leading economists, real estate experts and investment and market strategists to predict the path of the Zillow Home Value Index over the next five years. Zillow also sponsors the bi-annual Zillow Housing Confidence Index (ZHCI) which measures consumer confidence in local housing markets, both currently and over time. Launched in 2006, Zillow is owned and operated by Zillow Group (NASDAQ: Z), and headquartered in Seattle.

Zillow is a registered trademark of Zillow, Inc.

i Zillow determined affordability by analyzing the current percentage of a metro area's median income needed to afford the rent or the monthly mortgage payment on a median-priced home or apartment, and compared it to the share of income needed in the pre-bubble years between 1985 and 1999. For mortgage affordability, Zillow assumed a 20 percent down payment and a 30-year, fixed-rate mortgage at prevailing mortgage rates pulled from the Freddie Mac Primary Mortgage Market Survey. If the share of monthly income currently needed to afford the median-priced home or apartment is greater than it was during the pre-bubble years, that area is considered unaffordable for typical buyers or renters.

ii Zillow analyzed population and migration data from the U.S. Census Bureau and Moody's Analytics from 2012-2014 and the 2012-2013 Building Permits Survey, U.S. Census Bureau and U.S. Department of Housing and Urban Development. http://www.zillow.com/research/motivated-to-move-9127/

iii http://www.sfmayor.org/index.aspx?recordid=507&page=977

iv http://www.cityofboston.gov/dnd/pdfs/boston2030/Housing_A_Changing_City-Boston_2030_full_plan.pdf

v Zillow analysis of U.S. Census Bureau, Current Population Survey, March Supplement, 2014, made available by IPUMS-USA, University of Minnesota, www.ipums.org.

vi Renters could expect to spend 24.5 percent of their monthly income on a median-priced rental between 1985 and 1999. Now, they can expect to spend 30.1 percent. Homebuyers could expect to spend 21.4 percent of their monthly pay on a mortgage payment, compared to 15.3 percent now.

SOURCE Zillow

Share this article