Voss Capital Nominates Three Candidates for Griffon Corp. Board

Believes Griffon is Significantly Undervalued Due to Poor Corporate Governance, Egregious Management Compensation and Conglomerate Discount

Highlights Sustained Underperformance Vs Peer Group Over Past Decade

Urges Company to Explore All Potential Strategic Alternatives to Enhance Value for Shareholders

Nominates Highly Qualified Candidates to Bring Essential Expertise and New Perspectives, Position the Company for Future Success and Improve Oversight of Management

HOUSTON, Nov. 23, 2021 /PRNewswire/ -- Voss Capital, LLC (“Voss”), a significant shareholder of Griffon Corp. (NYSE: GFF) (“Griffon” or the “Company”) today issued a public letter to Griffon’s Board of Directors (the “Board”) and announced its nomination of three highly-qualified candidates – Gerry Bollman, H.C. Charles Diao and Leviathan Winn – for election as directors of the Company. The full text of the letter is below:

Dear Members of the Board:

As you know, Voss Capital, LLC (“Voss”) is a significant shareholder of Griffon Corp. (NYSE: GFF) (“Griffon” or the “Company”). In our private conversations with Griffon’s management and the Board, we have raised concerns about what we believe are significant, yet correctable, issues at the Company. Unfortunately, the Company has been dismissive and unreceptive during these discussions. We believe that Griffon has a collection of attractive businesses that is significantly undervalued in the public markets due to poor corporate governance, egregious management compensation and an outdated conglomerate structure.

While the Company announced elements of our proposed changes to corporate governance in conjunction with its Q4 2021 earnings release, these changes are not urgent enough nor do they go nearly far enough to rectify the existing deficiencies. Not only is the Company procrastinating long overdue governance changes that should be enacted immediately, but its announced changes do not address multiple remaining governance issues, such as the perceived lack of true Board independence and relevant expertise on the Board, a right sizing of management compensation and the urgently needed separation of the Chairman and CEO role.

The Company announced they are committed to increasing Board diversity by 2025 but has not provided any rationale as to why it will take so long. Voss has already privately nominated two highly qualified minority Board candidates that would add meaningful perspectives and expertise, in addition to improving the diversity of the Board, as soon as 2022. Furthermore, if the Company is truly committed to improving governance, the Board should be declassified right away – starting with the directors elected at the 2022 annual meeting.

In our view, the best way to remedy the perpetual conglomerate and governance discount to the Company’s stock is to take the following steps:

- Immediately refresh the Board with truly independent directors who will hold management accountable.

- Bring management compensation in-line with comps and base incentive pay on metrics which more accurately reflect value creation for shareholders (e.g., ROIC).

- Form an independent committee of the Board to conduct a comprehensive strategic review with the goal of maximizing shareholder value.

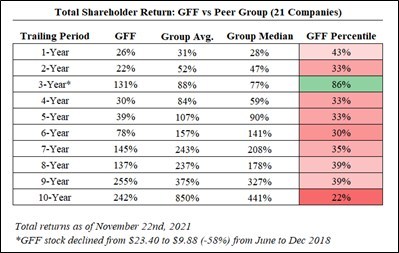

Griffon’s Persistent Underperformance and Lack of Value Creation

Over the past decade, Griffon’s total shareholder returns have significantly lagged those of its self-selected peer group, as illustrated in the below table.

[please refer to the Total Shareholder Return: GFF vs Peer Group (21 Companies) table]

Judging from the market’s poor reaction to this week’s earnings call where Mr. Kramer talked about conducting more M&A, it is clear investors have no confidence in this management team’s operational or capital allocation abilities. According to our calculations, the Company has failed to earn a return on invested capital that is above its cost of capital in 12 out of 13 years under Mr. Kramer’s tenure, thus continually destroying shareholder value.

[please refer to the Griffon’s Return on Invested Capital Below Average Cost of Capital During Ron Kramer’s Tenure graph]

Poor Corporate Governance

Griffon's Board is composed of 14 members, including two members of the management team: Mr. Kramer, who is also the Chairman, and COO Bob Mehmel. We seriously question the ability of this Board to operate objectively and truly hold management accountable while the CEO and COO are presiding over meetings. Our meeting with three “independent” directors, including the lead independent director, only reinforced this view given their clear deference to Mr. Kramer.

Furthermore, as currently composed, the Board has all the hallmarks of entrenchment: it is stale, predominantly male and long tenured. Half of the independent directors are over the age of 70 and nearly a third of the Board has served for over 10 years, including one 82-year-old member who has been a Board member for nearly 60 years. We also note that half of the Board has not bought a single share of Griffon stock the past five years, which we view as inexplicable, especially considering the attractive valuation of the stock, and an impediment to representing shareholder interests.

While the Company touts the Board’s 12 “independent” directors and emphasizes recent additions, the reality is very different. According to the Company’s proxy statement, Mr. Kramer has handpicked three of the last four "independent" directors, handing them three-year appointments that pay out approximately $200,000 per year. When we asked Mr. Kramer how the Company selected these new directors, he replied: “Well how do you pick your employees?” To us, this remark seems to be indicative of the boardroom environment and shows that Mr. Kramer does not fully understand the role of a board of directors. Griffon is a public company that is owned by its shareholders and Board members are not Mr. Kramer’s “employees”. Directors are elected by shareholders to oversee Mr. Kramer and the rest of his management team, not the other way around.

Additionally, we note that both the Board and the management team are largely comprised of people with military or casino backgrounds. This strikes us as odd, given that Griffon’s businesses have absolutely nothing to do with casinos or gaming, while less than 8% of the Company's earnings come from its defense business. To us, the only plausible explanation for this is that Mr. Kramer is filling the Board and management team with industry friends from his previous days at Wynn Resorts and calling them “independent.” Mr. Kramer’s apparent habit of selecting directors based on personal relationships rather than qualifications leaves the Company with a Board that entirely lacks directors with either building product or consumer tool experience, despite the fact that 92% of Griffon’s earnings come from those two industries. Moreover, we note the Board members with defense backgrounds will soon be redundant as directors, as the Company is actively exploring a sale of its Defense Electronics segment. Given the imminent spin-off of this business, we urge the Company to rationalize and reduce the Board size from an excessive 14 members to 12 directors, by removing Victor Renuart and Robert Harrison, whose military expertise will be irrelevant to a soon-to-be consumer and building products company.

Egregious Management Compensation

In what we consider a stunning example of how the Board has long failed to adequately assert its authority over management, Mr. Kramer and other executives routinely received outsized compensation packages. Over the past five years, Mr. Kramer has personally collected well over $60 million, and the top four executives combined have received over $100 million.

To put this in perspective, in 2020 Mr. Kramer was paid more than the CEOs of many of the largest, most profitable companies in the world including Starbucks, Disney and Home Depot, and nearly as much as the CEOs of Mastercard and Costco combined, despite GFF being 1/200th of the average size of these companies.

Comparing Mr. Kramer’s salary to CEOs of similar-sized public companies, i.e., those with market capitalizations in the $1 - $2 billion range, he is paid more than 417 of the 420 peers in this market cap range. Comparing Mr. Kramer’s compensation to the CEOs of the Company’s own selected peer group paints a similar picture. Mr. Kramer is paid more than any CEO in Griffon’s chosen peer group on a trailing 1-year, 3-year, 5-year, and 10-year average basis. In fact, his compensation represents a steadily increasing multiple of the group’s median, which is now in excess of 3.0x. Even worse, the Company has selected peer companies that have, on average, over three times Griffon’s market capitalization. On a size-adjusted basis Mr. Kramer is paid 9.1x the peer group average.

[please refer to the Griffon CEO Compensation vs Peer Group table]

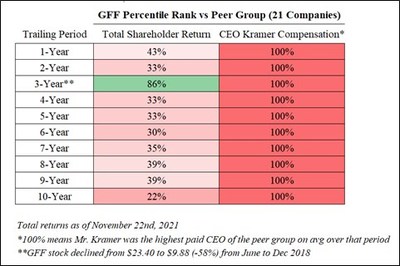

Paying a CEO many times what his peers make may be justified when the person delivers exceptional relative shareholder returns. Unfortunately, this is not the case with Mr. Kramer. As shown below, under Mr. Kramer’s tenure, GFF has remained in the bottom third in terms of shareholder returns relative to its own selected peer group in almost every measured period over the past ten years – falling into the bottom quartile since 2011.

[please refer to the GFF Percentile Rank vs Peer Group (21 Companies) table]

In other words, for a decade Mr. Kramer has been pocketing top-tier pay while producing bottom-tier returns for Griffon shareholders. Not surprisingly, in our meeting with the Board they were unable to defend or explain the outsized compensation with any empirical reasoning or logic.

Egregious pay like this raises other questions of excess at the company, such as why the company is paying over $150,000 per year for Mr. Kramer’s car and driver. This pattern of using company money to enrich the Kramer family tree is, unfortunately for shareholders, nothing new at Griffon. After his retirement from the CEO role in 2008, former Chairman Harvey Blau (Mr. Kramer’s father-in-law) was paid nearly $700,000 per year in “consulting fees” until 2018. All this excess and self-dealing would be well within Mr. Kramer’s right if Griffon was a privately owned company, but it is not. Griffon is a public company with shareholders and if he wishes to continue to use the company as his family’s personal piggy bank, as his family has done for decades, then we suggest he take the company private.

A Comprehensive Strategic Review is Needed

Griffon owns attractive businesses whose values are shrouded in an outdated conglomerate structure and diluted by poor corporate governance. Griffon’s inefficient corporate structure has no strategic rationale and its dissolvement provides a highly attractive opportunity for unlocking significant value for shareholders. While we see the Company’s exploration of a sale of its Defense Electronics business as a step in the right direction, we have identified potential for significantly more value creation in the remaining two business segments. The Home and Building Products segment and the Consumer and Professional Products segment have near zero operational overlap and would be easy to separate in a break-up scenario.

During one of our attempts to share our view on Griffon with Mr. Kramer, he admitted to us that the Home and Building Products business alone, if valued at the current average transaction multiple of 12x EBITDA, would recoup more than Griffon’s entire enterprise value. However, despite this admission, he claims that now is not the time to sell. Mr. Kramer also admitted that he has been receiving inbound calls from investment banks expressing interest in the Company’s businesses – something that, for some reason, seemed to annoy him. We are surprised, disappointed, and dismayed that the Chairman and CEO of a public company is annoyed by inbound M&A interest at valuations that are most likely well above current market value. To us, this is indicative of Mr. Kramer’s feudal approach to Griffon – he thinks that the Company belongs to him rather than its shareholders. If Mr. Kramer was focused on fulfilling his fiduciary duty to the Company’s actual owners, he would engage with anyone showing interest in acquiring Griffon’s largest segment. Instead, however, Mr. Kramer insisted to us that he wants to “be buying not selling", as he made clear again on the Q4 earnings call. We note that this statement is made at a time when the world is awash with money that needs to be deployed, and when valuations in many industries, including building products companies, are at all-time highs.

In fact, investment bank Harris Williams, a building products specialist, stated in July of this year:

“This is an ideal environment for [building products] sellers... Now is the time for building products and materials companies to take advantage of surging interest in the space... If going to market is on the agenda, companies should quickly take action… there is unlikely to be a better time to exit than right now.”1

It isn’t just in private that Mr. Kramer concedes he could unlock value for shareholders if the company was to conduct a strategic review. A Raymond James analyst described the Griffon management team’s remarks at a non-deal roadshow in May 2021 saying:

“[Management] concedes to a possible "conglomerate discount” … CEO Kramer suggested CPP (AMES) should warrant a 10x multiple (presumably based on both public and private market values) ... further, HBP/Clopay was argued to be valued "much" higher than CPP... DE/Telephonics was argued should be valued the "highest" multiple of the three."

We don’t disagree with the multiples Mr. Kramer is suggesting, which, if realized, would value GFF shares at well over $50 per share or >90% upside from the current share price. The only way Mr. Kramer can acknowledge the conglomerate discount, which is easily fixable, but also insist he doesn’t want to engage a bank to explore a break-up is if he wishes to continue to enrich himself personally at the shareholders’ expense.

Now is the optimal time for a committee of truly independent directors to conduct a comprehensive strategic review of all potential paths for unlocking shareholder value and we are highly confident there are several suitors who would be interested in a transaction for each of the three segments.

New Perspectives are Needed on the Board

For the reasons stated above, the Griffon Board must be refreshed with new, truly independent directors who have relevant experience and who will act with a sense of urgency to fully capitalize on the favorable industry dynamics and unlock the value of Griffon Corp’s underlying businesses. Our nominees would do just that.

Our nominees are:

Gerry Bollman – Mr. Bollman has more than a decade of experience in the building materials industry, most recently as Group Chief Financial Officer at Reliance Worldwide Corporation and Chief Financial Officer at Fletcher Building Limited, the largest building products company in New Zealand and the largest building products supplier to Australia. During his six-year tenure at Fletcher, Mr. Bollman also served as the Chief Executive of Strategy & Business Performance overseeing the company’s portfolio of 30 businesses and led a process to rationalize and sell non-core assets to maximize value. Earlier in his career, Mr. Bollman served as the Chief Financial Officer of Formica Corporation, a building products company acquired by Fletcher. Currently Mr. Bollman is the Chief Financial Officer at J&J Ventures Gaming, LLC, Illinois’ leading distributive gaming terminal operator. Mr. Bollman received an M.B.A. from the Stephen M. Ross School of Business at the University of Michigan and a B.S.B.A. in Finance from Xavier University.

H.C. Charles Diao – Mr. Diao is a former Senior Vice President of Finance, Corporate Development, and Corporate Treasurer of DXC Technology Company, one of the world’s largest IT services and technology solutions providers. He also served as DXC’s Chairman of the Corporate Finance Executive Committee and oversaw the acquisitions of Luxoft, Molina Medicaid Solutions, Xchanging plc, and the tax-free spin-offs of two federal government contractors to form CSRA Inc., and Perspecta Inc. During his time at DXC, he also oversaw the carve-out disposition of various units, including the nation’s largest Medicaid software solutions business. Mr. Diao currently serves on the Board of Directors of Turning Point Brands, Inc., where he is the Chairman of the Audit Committee and Member of the Nominating, Governance and ESG Committee. He previously served on the Board of Media General Inc. and was Chairman of its Nominating and Governance Committee and a member of the Audit Committee. Mr. Diao also has over 20 years of experience as an investment and merchant banker advising and executing an array of corporate actions, including segment spinoffs, acquisitions, and divestitures. Mr. Diao holds a B.S.E. from Princeton University and an M.B.A. from Harvard Business School.

Leviathan Winn – Mr. Winn is currently the Chief Financial Officer of Zulily, a subsidiary of Qurate Retail, Inc. Prior to Zulily, Mr. Winn served as the Chief Financial Officer of Qdoba Mexican Eats, a portfolio company of Apollo Global Management, and prior to that, Mr. Winn was a division Chief Financial Officer for Taco Bell Corporation, a subsidiary of Yum! Brands, Inc. Over the course of his career, he worked in various financial and strategic capacities, including serving as Head of Strategic Development in the consumer banking arm of JP Morgan Chase. Mr. Winn also worked at McKinsey & Company, where he advised global clients on corporate strategy, transformation, M&A and restructuring transactions. He received his undergraduate degree in finance from Texas A&M University and earned his MBA from The Wharton School at the University of Pennsylvania.

We look forward to continuing to engage with Griffon and its shareholders to enhance value at the Company.

Sincerely,

Travis Cocke

Chief Investment Officer

Voss Capital

Media Contact:

Serena Koontz

Head of Investor Relations

Voss Capital, LLC

[email protected]

CERTAIN INFORMATION CONCERNING THE PARTICIPANTS

Voss Value Master Fund, LP, a Cayman Islands limited partnership (“Voss Value Master Fund”), together with the other participants named herein (collectively, “Voss”), intends to file a preliminary proxy statement and accompanying proxy card with the Securities and Exchange Commission (“SEC”) to be used to solicit votes for the election of its slate of highly-qualified director nominees at the 2022 annual meeting of stockholders of Griffon Corporation, a Delaware corporation (the “Company”).

VOSS STRONGLY ADVISES ALL STOCKHOLDERS OF THE COMPANY TO READ THE PROXY STATEMENT AND OTHER PROXY MATERIALS AS THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. SUCH PROXY MATERIALS WILL BE AVAILABLE AT NO CHARGE ON THE SEC'S WEB SITE AT HTTP://WWW.SEC.GOV. IN ADDITION, THE PARTICIPANTS IN THIS PROXY SOLICITATION WILL PROVIDE COPIES OF THE PROXY STATEMENT WITHOUT CHARGE, WHEN AVAILABLE, UPON REQUEST.

The participants in the proxy solicitation are anticipated to be Voss Value Master Fund, Voss Value-Oriented Special Situation Fund, LP, a Delaware limited partnership (“Voss Value Special Situations Fund”), Voss Advisors GP, LLC, a Texas limited liability company (“Voss GP”), Voss Capital, LLC, a Texas limited liability company (“Voss Capital”), Travis W. Cocke, Gerry Bollman, H. C. Charles Diao and Leviathan Winn.

As of the date hereof, Voss Value Master Fund directly beneficially owns 711,320 shares of Common Stock, par value $0.25 per share, of the Company (the “Common Stock”), including 1,000 shares of Common Stock held in record name. As of the date hereof, Voss Value Special Situations Fund directly beneficially owns 128,358 shares of Common Stock. As the general partner of Voss Value Master Fund and Voss Value Special Situations Fund, Voss GP may be deemed to beneficially own the 839,678 shares of Common Stock beneficially owned in the aggregate by Voss Value Master Fund and Voss Value Special Situations Fund. As the investment manager of Voss Value Master Fund, Voss Value Special Situations Fund and a certain separately managed account (the “Voss Managed Account”), Voss Capital may be deemed to beneficially own the 1,192,409 shares of Common Stock beneficially owned in the aggregate by Voss Value Master Fund and Voss Value Special Situations and held in the Voss Managed Account. As the managing member of Voss Capital and Voss GP, Mr. Cocke may be deemed to beneficially own the 1,192,409 shares of Common Stock beneficially owned in the aggregate by Voss Value Master Fund and Voss Value Special Situations and held in the Voss Managed Account. As of the date hereof, none of Messrs. Bollman, Diao or Winn own beneficially or of record any securities of the Company.

1 https://www.harriswilliams.com/article/exit-now-data-shows-opportunity-building-products-company-owners

SOURCE Voss Capital

Share this article