VantageScore CreditGauge™ January 2024: Consumer Credit Delinquencies Climbed in January as More Consumers Dropped to VantageScore Subprime Credit Tier

- Delinquencies Up in January 2024 Across All Products and VantageScore Credit Tiers Compared to January 2023

- The Number of Consumers in the VantageScore Prime Credit Tier Decreased By 1% as Stressed Borrowers' Credit Quality Declined

- New Account Originations Slowed Across All Products; Banks and Credit Card Lenders "Pumped the Brakes" on New Lending

SAN FRANCISCO, Feb. 27, 2024 /PRNewswire/ -- VantageScore, the leading national credit-scoring and data analytics company, today released its January 2024 CreditGauge, a monthly analysis highlighting the overall health of U.S. consumer credit. The average VantageScore 4.0 credit score remained at 701. The lowest VantageScore 4.0 credit score is 300, while the highest score is 850. In January, delinquencies spiked to the highest level in nearly four years as some consumers dropped out of the VantageScore Prime credit tier into VantageScore Subprime due to inflation-induced economic stress. In contrast, some consumers moved up from the VantageScore Prime credit tier to VantageScore Superprime, an indication of two very different consumer segments. Consumers with higher credit scores continued to do well, while those with lower credit scores faced growing economic pressures. Banks and lenders tightened new account originations for the first time in several months as credit quality concerns grew.

Key findings for January 2024 CreditGauge data include:

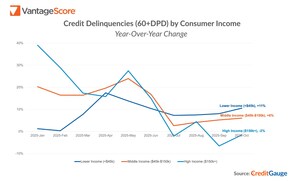

DELINQUENCIES ROSE ACROSS ALL CREDIT SEGMENTS – Delinquencies climbed across all VantageScore credit tiers and products in January 2024 (Auto Loan, Credit Card, Mortgage, and Personal Loan). Overall early-stage delinquencies increased 0.9 points from 0.89% in December 2023 to 0.98% in January 2024. This was the second-largest monthly increase in the last four years to the highest level since February 2020. Delinquencies also rose compared to December 2023 in 60-89 DPD (Days Past Due) and 90-119 DPD categories. In addition, overall balances reached a new high in January 2024 at $104,622, an increase of 1.8% year-over-year. Credit utilization dipped slightly (-0.1%) for the month. Borrowers across all credit products demonstrated a higher level of economic stress in January, in part a result of sustained inflation and moderately worsening employment levels.

VANTAGESCORE PRIME CREDIT TIER SHRANK – In January, there was a 1% decline in the VantageScore Prime credit tier as consumers migrated to both Superprime (+0.7%) and Subprime (+0.3%) tiers. The drop in the VantageScore Prime credit tier was due to very different economic experiences. Year-over-year, consumers with higher credit scores continued to meet their debt obligations, which caused the Superprime population to increase. On the other hand, consumers with lower VantageScore credit scores remained stressed as the VantageScore Subprime credit tier grew.

NEW ACCOUNT ORIGINATIONS SLOWED ACROSS ALL PRODUCTS – New account originations declined across all products in January 2024 compared to December 2023. New account originations also declined across all products year-over-year. Credit Card originations, after rising each month during the fourth quarter of 2023, from 3.09% to 3.53%, fell the most in January 2024 compared to December 2023, down 0.38%. This reflected the seasonal lending pullback post-holidays. Auto Loan and Mortgage originations saw their fourth consecutive month of decline, with Auto Loans decreasing by 0.09% and Mortgages by 0.03%.

"Consumers are struggling with higher credit balances and falling behind on paying their bills, in part due to sustained inflation," said Susan Fahy, Executive Vice President and Chief Digital Officer at VantageScore. "With the Fed indicating that they are unlikely to cut rates soon, both lenders and consumers will need to remain vigilant in managing credit levels."

To view the full CreditGauge report, visit the VantageScore website.

About VantageScore CreditGauge™

CreditGauge is provided both as a monthly report to industry stakeholders as well as through a series of interactive tools at VantageScore.com. Stakeholders can use the tools to execute additional queries on credit metrics and compare current levels to a pre-pandemic timeframe, starting with January 2020. CreditGauge represents the views and opinions of VantageScore and does not necessarily reflect or represent the views of the Nationwide Credit Reporting Agencies (NCRAs)-- Equifax, Experian, and TransUnion.

VantageScore CreditGauge content, including any estimated economic forecasts, is intended for informational purposes only. VantageScore is not responsible for the use of the information contained in the CreditGauge report, including any assumptions or conclusions drawn from its use.

VantageScore CreditGauge is part of a suite of digital tools available on VantageScore.com, which also includes Inclusion360™, RiskRatio™, and MarketGain™.

About VantageScore®

VantageScore is a leading credit-score model development company that generates the most inclusive, innovative, and predictive models used in the consumer-credit marketplace. VantageScore is used by 8 out of the top ten banks in the U.S. and more than 3,000 fintechs and consumer websites. In 2023 over 19 billion VantageScore credit scores were used to assess people for credit products like auto loans, personal loans and mortgages, representing a 30% increase over 2022.

VantageScore is an independently managed joint venture company of the three Nationwide Credit Reporting Agencies (NCRAs)-- Equifax, Experian, and TransUnion.

SOURCE VantageScore

Share this article