Granite Issues Letter to Unitholders

- Highlights Granite's strong performance and prospects

- Warns unitholders of dissidents' short-term strategy, poor track records in the real estate sector and history of related party transactions

- Reminds unitholders to vote only the WHITE proxy FOR Granite's nominees, well in advance of the proxy voting deadline of 10:00 a.m. (Toronto time) on Tuesday, June 13, 2017

TORONTO, May 30, 2017 /PRNewswire/ - Granite Real Estate Investment Trust ("Granite REIT") and Granite REIT Inc. ("Granite GP", and together with Granite REIT, "Granite") (TSX: GRT.UN; NYSE: GRP.U) has issued a letter to unitholders, urging them to protect their investment from FrontFour Capital and Sandpiper Group by voting only the WHITE proxy FOR Granite's nominees, well in advance of the proxy voting deadline of 10:00 a.m. (Toronto time) on Tuesday, June 13, 2017.

The full contents of the letter are included below:

May 30, 2017

Dear Granite Unitholders:

Earlier this month, two dissident unitholders – FrontFour Capital and Sandpiper Group – publicly attacked Granite's track record, despite it being one of the best-performing REITs in Canada. At the time, a leading independent equity research analyst said:

"…we take issue with the far too one-sided, and in some instances, aggressive tone of the [FrontFour-Sandpiper] presentation. In this regard, the FrontFour-Sandpiper presentation seemingly fails to give management and the board credit for the many positive things that have been achieved over the past five years." – RBC Capital Markets (May 11, 2017).

Granite further set the record straight by issuing a letter and proxy circular that highlighted how the Board and management have executed a strategy that has driven significant gains for Granite unitholders and positioned Granite for continued success in 2017 and beyond. That strategy has involved a board renewal process that began last year, described by another independent equity research analyst as follows:

"Granite nominated two highly qualified and experienced independent Trustees to its Board: Remco Daal (President of Cdn. Real Estate, QuadReal Property Group); and Kelly Marshall (Managing Partner, Corporate Finance, Brookfield Asset Mgmt.). This follows the appointment of two additional highly qualified Trustees last year - Brydon Cruise (Chairman and Managing Partner, Brookfield Financial) and Donald Clow (CEO, Crombie REIT)...Granite intends to continue its Board renewal process into 2018 and beyond. The moves thus far should serve the REIT well and inspire additional investor confidence, in our view." – (TD Securities (May 17, 2017) (emphasis added)

Now, less than three weeks before the scheduled date of Granite's annual meeting, the dissidents have put forward three nominees for election to Granite's Board. Unitholders are urged to vote only the WHITE proxy FOR Granite's nominees, well in advance of the proxy voting deadline of 10:00 a.m. (Toronto time) on Tuesday, June 13, 2017.

We have written this letter, and provided the views of respected independent equity research analysts, to help you see through the dissidents' disingenuous statements – and to set the record straight. In this letter, we highlight:

- Granite's strong performance and prospects under your current Board and management;

- that the dissidents have been disingenuous and should not be trusted by unitholders;

- the dissidents' short-term strategy and poor track records in the real estate sector; and

- that the dissidents' nominees have presided over related party transactions and are unsuitable to represent the interests of all unitholders.

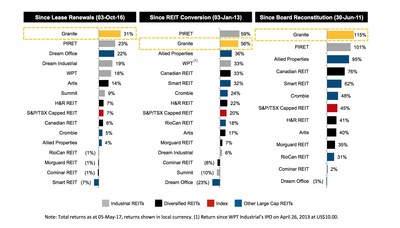

The first and most fundamental issue is this: Granite is one of the best performing REITs in Canada.

Moreover, Granite has taken the necessary actions, in an effective and disciplined way, to create a strong platform for accelerated growth.

The dissidents have tried to make you believe that what you see in the chart above isn't true by devising a misleading peer group to support their faulty narrative. We exposed their tactic, and having been called out, the dissidents conspicuously changed their so-called peer group to the Bloomberg REIT Industrial/Warehouse Index. But yet again, the dissidents have made an inappropriate comparison in comparing Granite's performance to that of a U.S. index, because Granite derives only approximately 29% of its revenues from the U.S. Granite earns approximately 45% of its revenues from Europe and approximately 26% of its revenues from Canada. The market fundamentals in both of these regions are different than those in the U.S. Here is what an independent equity research analyst had to say about Granite's performance:

"… Granite's units have earned a cumulative five-year return of 97%, substantially in excess of the 32% from the S&P/TSX Capped REIT Index. And, interestingly, Granite REIT has posted significant outperformance versus the S&P/TSX Capped REIT Index on a one-, three- and five-year basis." – RBC Capital Markets (May 11, 2017)

The dissidents have also tried to take credit for Granite's recent strong unit price performance while intentionally ignoring the significantly positive impact of the Magna lease renewals on Granite. Here is what another independent equity research analyst says on the matter:

"With respect to the unit price, we believe management has had a direct hand in the recent outperformance and unitholder value creation via the significant de-risking accomplished through the Magna lease extensions in October 2016 and the December 2016 issuance of its Series 3 unsecured debentures which reduced its cost of capital and extended debt duration." – Scotia Capital (May 17, 2017)

Granite continues to execute its strategy

The dissidents have doubled down on their initial rhetoric regarding Granite's strategy and execution. Again, don't take our word for it. Here is what another independent equity research analyst thinks:

"FF/S [the dissidents] has not adequately argued their case. Granite is a work-in-progress, more so than many other companies, but this is largely because of its origins. Significant progress has already been made, and we firmly believe that further positive initiatives are underway. With much heavy-lifting done on the risk side, and with the CEO position filled and strategic review completed, we look forward with increased confidence that Granite will put its balance sheet to work in a disciplined and accretive manner." – TD Securities (May 17, 2017)

Granite's track record is clear and independent equity research analysts have seen through the dissidents' "alternative facts". In reality, what the dissidents attempt to paint as a deficiency, third-party equity research analysts view as a vital strength:

"In our view, the greatest long-term wealth creation in the listed property sector comes from REITs that are: 1) methodical in their execution; 2) sticklers for not diluting unitholders; and, 3) demonstrated stewards of their unitholders' capital. Today, Granite REIT continues to have the advantage of the lowest gearing of any Canadian REIT. We see Granite's low financial leverage not as some sort of problem or indication of a company "plagued by inaction" or "strategic failures". Instead, we see the REIT's significant balance sheet capacity as one of its greatest strengths" – RBC Capital Markets (May 11, 2017) (emphasis added)

The dissidents have been disingenuous and should not be trusted by unitholders

The dissidents have also made a number of new false or contradictory statements to achieve their objectives. This is completely at odds with Granite's culture and what Granite's unitholders should expect from their Board members. To note just a few concerning statements:

- Failed settlement discussions. In their circular, the dissidents claim that Granite "rejected a very reasonable and fair settlement offer …". The truth is that after advising Granite in early May that their Board nominees would be Zach George and Samir Manji, the dissidents provided no further information to Granite. There was no further contact until weeks later, when a significant unitholder asked to meet with us on May 24, 2017. A proposal was made to us by the unitholder at that meeting in an attempt to resolve the issues that exist between the Granite Board and the dissidents. A revised version of that proposal, which we learned had the backing of the dissidents, was considered by the Granite Board and unanimously rejected. The proposal was not fair, reasonable or in the best interests of unitholders, and would have, we believe, undermined the effective functioning of the Granite Board.

- False claims regarding an external management structure. In their circular, the dissidents imply that Granite has considered the externalization of its management. This is a baseless fabrication that is meant to alarm unitholders. None of Granite's Board members or management have ever discussed an external management structure for Granite, nor is such a structure being considered.

- Erroneously attacking the strong track records of Mr. Voorheis and Mr. Dey. Both individuals have been appointed to the boards of companies that were widely known to be in difficult situations. They were appointed to these boards specifically because of their outstanding expertise and governance credentials. The dissidents are incorrect in suggesting Mr. Dey and Mr. Voorheis were responsible for creating the challenges these companies faced, when in fact they were brought in to address them. The dissidents also state that Mr. Voorheis purchased units at a discounted price in a blackout period. Neither of these assertions is true.

- Continued mischaracterization of Granite's successful strategic review. Quite the opposite of being the failure that the dissidents claim, the strategic review reaffirmed that the Board's current strategy offered the greatest value to unitholders. That decision has since been validated by Granite's performance. Since the completion of the strategic review in March 2016, Granite has returned 38%, compared to 16% for the S&P/TSX Capped REIT Index, and has eliminated the discount to consensus net asset value per unit. Granite's current unit price is significantly higher than the price offered under any acquisition proposal received or any alternative pursued by Granite during the review process. The course of action adopted by the Board as a result of the strategic review has clearly been successful and in unitholders' best interests.

- Dissidents' stance on Granite's costs. In their recent communications, the dissidents express concern regarding Granite's costs, but ignore key facts. For example:

"Granite has also reduced its Board compensation rates by 20% - 47% (see exhibit), based on less expected time commitment going forward" – TD Securities (May 17, 2017)

The dissidents also fail to acknowledge that Granite includes almost all management costs in its G&A expenses and does not reallocate or capitalize any management costs, which other REITs typically do. Granite's level of management expenses is well aligned with those of other industrial and international Canadian REITs. It is interesting that despite the dissidents' focus on cost reduction, their settlement demands included that Granite pay the unspecified, uncapped costs of their legal counsel, financial advisor and proxy solicitor. The dissidents do appear to be focused on managing their own costs, but with Granite's cash at the expense of our unitholders.

The dissidents have a track record of value destruction and a short-term orientation

FrontFour entities have underperformed

In the dissidents' circular, FrontFour makes statements regarding entities it has controlled in the real estate sector using returns for highly selective periods. Here are the facts:

- For the entire period FrontFour's principal was on the board of Huntingdon until the announcement of the transaction with IAT Cargo, Huntingdon underperformed the index by 48%

- For the entire period FrontFour's principal was on the board of Huntingdon until the announcement of the transaction with Slate, Huntingdon underperformed the index by 9% per annum

- For the entire period FrontFour's principal was on the board of IAT Cargo until the announcement of the Huntingdon transaction, IAT Cargo underperformed the index by 15%

FrontFour has also not addressed the claim that its assets under management have suffered a significant decline, with public sources showing that their assets under management have dropped by more than 27%, from approximately U.S.$430 million to approximately U.S.$310 million over the last couple of years. If FrontFour's own investors no longer want to invest with them, why should you have faith in them?

FrontFour's short-term strategy

The dissidents claim to be long-term investors. In its circular, Granite highlighted that FrontFour has a history of short-term investments, with an average investment holding period of approximately three quarters, and that a material portion of its position in Granite is held in call options, which expire shortly after Granite's annual meeting and would benefit from a short-term pop in the unit price.

The dissident nominees are unsuitable to represent the interests of all unitholders on your Board

Sandpiper principal and dissident nominee Samir Manji and dissident nominee Al Mawani have a history of related party transactions and have overseen poor performance in the real estate sector. Mr. Manji was Amica Mature Lifestyles' CEO while Mr. Mawani was a director on its board for a period of six years.

While the dissident nominees failed to drive performance at Amica, they were party to a series of related party transactions with the Manji family, including co-investments, loans, loan forgiveness and acquisitions of interests in entities controlled by the Manji family. Mr. Mawani reviewed and approved related party transactions with entities controlled by the Manji family in his capacity as a member of Amica's Investment Committee and as an Amica director.

The dissidents buried in the back of their proxy circular information that their third nominee, Peter Aghar, is a trustee of PRO REIT, despite prominently highlighting the public company board directorship of another one of their nominees in their May 26, 2017 press release. PRO REIT entered into a Strategic Investment Agreement with Lotus Crux, which is a partnership between Lotus Pacific and Crux Capital, an entity controlled by Mr. Aghar. The Agreement provides an incentive for Mr. Aghar, in his capacity as a trustee of PRO REIT, to pursue related party acquisitions with Lotus Crux. PRO REIT has acquired seven properties from Lotus Crux, all related party transactions, resulting in approximately C$550,000 of additional fees for Lotus Crux.

Mr. Manji's, Mr. Mawani's and Mr. Aghar's track records of poor performance and related-party transactions suggest that they would not represent the best long-term interests of all Granite unitholders if elected to the Board.

Vote only the WHITE proxy to continue Granite's proven strategy for value creation

Granite continues to engage with its unitholders and is gratified by the high levels of support received relating to Granite's strategy and the current management team and Board responsible for executing this strategy. Granite is one of the best-performing REITs in Canada, has strong corporate governance, and is well positioned to pursue its acquisition strategy. Do not let disingenuous, short-term oriented dissidents with a history of value destruction jeopardize your investment. Unitholders are urged to vote only the WHITE proxy FOR Granite's nominees, well in advance of the proxy voting deadline of 10:00 a.m. (Toronto time) on Tuesday, June 13, 2017.

Thank you for your continued trust in and support of Granite.

//signed//

G. WESLEY VOORHEIS

Chairman,

Granite Real Estate Investment Trust and

Granite REIT Inc.

//signed//

MICHAEL FORSAYETH

Chief Executive Officer,

Granite Real Estate Investment Trust and

Granite REIT Inc.

Copies of the letter and proxy circular are available on Granite's website at www.granite.com and filed on SEDAR at www.sedar.com.

ABOUT GRANITE

Granite is a Canadian-based REIT engaged in the ownership and management of predominantly industrial, warehouse and logistics properties in North America and Europe. Granite owns approximately 30 million square feet in over 90 rental income properties. Our tenant base includes Magna International Inc. and its operating subsidiaries as our largest tenants, in addition to tenants from other industries.

OTHER INFORMATION

Copies of financial data and other publicly filed documents are available through the internet on the Canadian Securities Administrators' Systems for Electronic Document Analysis and Retrieval (SEDAR) which can be accessed at www.sedar.com and on the United States Securities and Exchange Commission's Electronic Data Gathering, Analysis and Retrieval System (EDGAR) which can be accessed at www.sec.gov.

FORWARD-LOOKING STATEMENTS

This press release may contain statements that, to the extent they are not recitations of historical fact, constitute ''forward-looking statements'' or "forward-looking information" within the meaning of applicable securities legislation, including the United States Securities Act of 1933, as amended, the United States Securities Exchange Act of 1934, as amended, and applicable Canadian securities legislation. Forward-looking statements and forward-looking information may include, among others, statements regarding Granite's future plans, goals, strategies, intentions, beliefs, estimates, costs, objectives, economic performance, expectations, or foresight or the assumptions underlying any of the foregoing. Words such as "may", "would", "could", "will", "likely", "expect", "anticipate", "believe", "intend", "plan", "forecast", "project", "estimate", "seek" and similar expressions are used to identify forward-looking statements and forward-looking information.

Forward-looking statements and forward-looking information should not be read as guarantees of future events, performance or results and will not necessarily be accurate indications of whether or the times at or by which such future events or performance will be achieved. Undue reliance should not be placed on such statements. Forward-looking statements and forward-looking information are based on information available at the time and/or management's good faith assumptions and analyses made in light of its perception of historical trends, current conditions and expected future developments, as well as other factors management believes are appropriate in the circumstances, and are subject to known and unknown risks, uncertainties and other unpredictable factors, many of which are beyond Granite's control, that could cause actual events or results to differ materially from such forward-looking statements and forward-looking information. Important factors that could cause such differences include, but are not limited to economic, market and competitive conditions, and the risks set forth in the annual information form of Granite REIT and Granite REIT Inc. dated March 1, 2017 (the "Annual Information Form"). The "Risk Factors" section of the Annual Information Form also contains information about the material factors or assumptions underlying such forward-looking statements and forward-looking information. Forward-looking statements and forward-looking information speak only as of the date the statements and information were made and unless otherwise required by applicable securities laws, Granite expressly disclaims any intention and undertakes no obligation to update or revise any forward-looking statements or forward-looking information contained in this press release to reflect subsequent information, events or circumstances or otherwise.

For more information:

Unitholders

D.F. King at 1-866-822-1237 (toll free in North America) or 1-201-806-7301 (outside North America) or email at [email protected]

Michael Forsayeth, Chief Executive Officer, at 647-925-7600 or

Ilias Konstantopoulos, Chief Financial Officer, at 647-925-7540

Media

Joel Shaffer, Longview Communications

416-649-8006

SOURCE Granite Real Estate Investment Trust

Share this article