GOL announces information about the Corporate Reorganization

SAO PAULO, Feb. 12, 2021 /PRNewswire/ -- GOL Linhas Aéreas Inteligentes S.A. ("GOL") (NYSE: GOL and B3: GOLL4), Brazil's #1 domestic airline, pursuant to paragraph 4 of Article 157 of Law No. 6,404, dated December 15, 1976, as amended ("Brazilian Corporate Law"), CVM Instruction No. 358/2002 ("ICVM 358") and CVM Instruction No. 565/2014 ("ICVM 565"), hereby inform that, on the date hereof, a shareholders' meeting has been called to pass a resolution on the corporate reorganization (disclosed in GOL's material facts dated December 7, 2020 and January 18, 2021), as detailed below ("Reorganization").

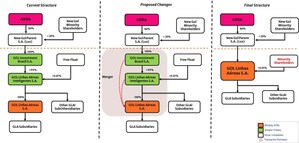

1. COMPANIES INVOLVED IN THE TRANSACTION AND THEIR ACTIVITIES

1.1. GOL

(a) Identification. GOL Linhas Aéreas Inteligentes S.A., a publicly-held company headquartered in the city of São Paulo, state of São Paulo, at Praça Comandante Lineu Gomes, S/N, Portaria 3, Jardim Aeroporto, 04626-020, enrolled with the Corporate Taxpayers' Registry (CNPJ/MF) under No. 06.164.253/0001-87.

(b) Activities. GOL's main corporate purpose is to exercise control over GOL Linhas Aéreas S.A. ("GLA"), whose main activities are air passenger, cargo or mail transportation, services in Brazil and abroad. Additionally, GOL also holds control over SMILES, whose main activity is the management of the SMILES Program, a coalition program.

1.2. SMILES

(a) Identification. Smiles Fidelidade S.A., a publicly-held company headquartered in the city of Barueri, state of São Paulo, at Alameda Rio Negro, 585, Edifício Padauiri, Bloco B, 2nd floor, suites 21 and 22, Alphaville, 06454-000, enrolled with the Corporate Taxpayers' Registry (CNPJ/MF) under No. 05.730.375/0001-20.

(b) Activities. SMILES's main corporate purpose is to manage SMILES Program, a coalition program. SMILES's business model is based on the development of a "pure" coalition program, comprising a single platform for the accrual and redemption of mileage, through a wide network of commercial and financial partners; SMILES's main commercial partner is GLA.

1.3. GLA

(a) Identification. GOL Linhas Aéreas S.A., a privately-held company headquartered in the city of Rio de Janeiro, state of Rio de Janeiro, at Praça Senador Salgado Filho, S/N, Aeroporto Santos Dumont, ground floor, public area, between hubs 46-48/O-P, Back Office Management Room, 20021-340, enrolled with the Corporate Taxpayers' Registry (CNPJ/MF) under No. 07.575.651/0001-59.

(b) Activities. GLA's main activities are air passenger, cargo or mail transportation, services in Brazil and abroad, and other connected, related or complementary air transportation activities, including, for example, passenger freight, own and third-party aircraft maintenance and repair services, and aircraft hangar services.

2. DESCRIPTION AND PURPOSE OF THE TRANSACTION

2.1. Description.

The Reorganization includes the following steps, which will be implemented simultaneously and interdependently, whose completion will be subject to the applicable corporate approvals and the approval of the majority of holders of SMILES outstanding shares:

(i) merger of SMILES common shares by GLA, for their market value, with GLA's issuance of common shares ("GLA Common Shares"), redeemable class B preferred shares ("GLA Redeemable Class B Preferred Shares") and redeemable class C preferred shares ("GLA Redeemable Class C Preferred Shares," together with the GLA Redeemable Class B Preferred Shares, "GLA Redeemable Preferred Shares") to SMILES shareholders ("Merger of SMILES Shares");

(ii) merger of GLA shares by GOL, for their economic value, with GOL's issuance of GOL preferred shares ("GOL Preferred Shares"), redeemable class B preferred shares ("GOL Redeemable Class B Preferred Shares") and redeemable class C preferred shares ("GOL Redeemable Class C Preferred Shares," together with the GOL Redeemable Class B Preferred Shares, "GOL Redeemable Preferred Shares") to GLA shareholders ("Merger of GOL Shares"); and

(iii) redemption of GLA Redeemable Preferred Shares and GOL Redeemable Preferred Shares, with payment in cash based on the redemption of GOL Redeemable Preferred Shares to SMILES shareholders to be made on the Date of Settlement ("Redemption").

GOL clarifies that adjustments have been made in the structure described in the Material Fact disclosed on December 7, 2020, notably in relation to: the establishment of only two exchange ratios, as described in item 4 below. However, the financial conditions previously announced have been fully maintained, particularly with regard to the implicit exchange ratio on which the proposal was based, of 0.825 GOL preferred share for each single common share issued by Smiles.

2.2. Purpose of the Transaction.

The purpose of the Reorganization is to migrate SMILES's shareholder base to GOL. Assuming that: (i) SMILES's total capital stock is represented, as of the Date of Consummation of the Reorganization (as defined below), by 124,158,953 common shares, excluding treasury shares and the shares vested under stock option plans; (ii) GLA's total capital stock is represented, as of the Date of Consummation of the Reorganization, by 1,915,298,982 common shares, and 701,729,152 preferred shares, excluding treasury shares; and (iii) GOL's total capital stock is represented, as of the Date of Consummation of the Reorganization, by 2,863,682,710 common shares and 272,200,223 preferred shares, excluding treasury shares and the shares vested under stock option plans; SMILES shareholders will receive, for each common share issued by SMILES held by them as of such date:

(i) (a) an amount in Brazilian currency of R$4.46 (related to the redemption of the GOL Redeemable Class B Preferred Shares), adjusted in accordance with the Protocol and Justification proposed by the management of GOL ("Protocol and Justification"), to be paid in cash, in a single installment, within ten business days from the Date of Consummation of the Reorganization ("Date of Financial Settlement"); and (b) 0.6601 preferred share issued by GOL ("Base Exchange Ratio"), adjusted in accordance with the Protocol and Justification; or

(ii) (a) an amount in Brazilian currency of R$17.86 (related to the redemption of the GOL Redeemable Class C Preferred Shares), adjusted in accordance with the Protocol and Justification, to be paid in cash, in a single installment, on the Financial Settlement Date; and (b) 0.1650 preferred share issued by GOL ("Optional Exchange Ratio"), adjusted in accordance with the Protocol and Justification, at the discretion of SMILES shareholders that, in the latter case, must exercise the option within the period to be timely disclosed through a Notice to Shareholders, if the Reorganization is approved.

GOL and GLA will take into account the amount of R$27.05 per GOL share and R$22.32 per SMILES share to determine the proposed exchange ratio. As described in the Protocol and Justification, the amounts described above will be proportionately adjusted by any stock splits, reverse stock splits, share dividend bonuses, interest on shareholders' equity or capital decreases of the companies as of the date hereof until the Date of Consummation of the Reorganization, subject to item 4.2 below. Any dividends, interest on shareholders' equity or capital decreases to be distributed to SMILES shareholders between the date hereof and the Date of Consummation of the Reorganization, as well as any withheld income tax due as a result of the Reorganization, when applicable and in accordance with applicable law, as described in item 4.3, will be proportionately deducted from the domestic currency portion of the Base Exchange List or the Optional Exchange List when implementing the Preferred Share Redemption described below.

GOL may, unilaterally and without the need to amend the Protocol and Justification, increase the redemption value of the shares and/or the number of shares to be received by investors in the Base Exchange Ratio or the Optional Exchange Ratio (always in proportion to the two options), without a decrease, in any case, in the total value to be received by investors, observing the adjustments foreseen in the Protocol and Justification.

3. MAIN BENEFITS, COSTS AND RISKS OF THE TRANSACTION

3.1. Main Benefits.

Historically and globally, the leading loyalty programs are controlled and managed by airlines. Airline tickets are consistently the most important reward category demanded by loyalty program members. The Group comprises the leading domestic players in the airline and loyalty program markets in Brazil, with a share of approximately 38% of the Brazilian aviation market and a share greater than 40% of the Brazilian loyalty program market.

In Brazil, competition in both the airline and loyalty program markets has become increasingly challenging in recent years. Loyalty programs have faced significant redemption cost increases due to, among other factors, higher occupancy rates of Brazilian airlines and increased competition from bank and credit card loyalty programs, which have offered more appealing redemption possibilities, such as more available seats for more travel destinations. Additionally, the credit card market, the main source of funds for loyalty programs, is stagnant and financial market deregulation with the entry of new players, such as fintechs, has affected the budgets of major credit card-issuing banks and put pressure on the prices of points of all loyalty programs in the Brazilian market.

The Group has made strong and coordinated efforts to increase the attractiveness of GLA's airline products and SMILES's loyalty program for its clients and partners. Nonetheless, distinct governance structures and shareholder bases have presented challenges to the Group in making necessary investments and coordinating the development of more competitive products and services. While this structure has become a burden to the Group as a whole, it has mainly affected the Group's loyalty program business because the structure does not allow sufficient agility and the managerial integration needed to compete in the current market reality.

In this context, the Group has concluded that the maintenance of separate corporate structures among the Group's businesses is not in the best interest of its shareholders.

Accordingly, the Reorganization seeks to:

- ensure the Group's long-term competitiveness in both of its key markets (airline travel and loyalty programs);

- unify GOL's and SMILES's shareholder bases, which will simplify the Group's shareholding structure, align shareholder interests and increase the market liquidity of the Group's shares;

- achieve improved, more efficient governance and decision making, through increased management coordination, a shared business plan and aligned goals within the Group;

- fully integrate (as opposed to merely consolidate) the financial and operational results, balance sheets and cash flows of SMILES, GLA and GOL to permit the Group to optimize its capital structure, cost of capital and financing sources, allowing the airline business to compete more effectively and the loyalty program business to benefit from the improved market position of its key business partner;

- strengthen the capital structure of the airline business; and

- realize synergies, achieving a more dynamic and flexible revenue management, and terminate tax inefficiencies.

3.2. Costs.

The managements of GOL and GLA estimate that the costs of the Reorganization will total, for both companies, approximately R$12,338,000, including expenses with publication, auditors, appraisers, legal counsel and other professionals engaged to advise on the Reorganization.

The management of SMILES estimates that the costs of the Reorganization will total, for SMILES, approximately R$7,253,000, including expenses with publication, auditors, appraisers, legal counsel and other professionals engaged to advise on the Reorganization.

3.3. Risks of the Transaction.

The management of GOL does not expect material risks in the implementation of the Reorganization, in addition to those that are usual for the day-to-day activities of the involved companies and compatible with the companies' sizes and operations.

The market value of GOL shares may vary at the time of completion of the Reorganization due to a number of factors that are beyond the control of the involved companies.

The success of the transaction will partially depend on the ability of the managements of the involved companies to create opportunities, economies and new businesses from the combination of activities and synergy generated by the unification of the shareholder bases of the companies. However, no assurance can be given that these opportunities and economies will be successful. If these objectives are not successfully achieved, the benefits expected from the Reorganization may not fully occur or may take longer than expected to occur.

4. SHARE EXCHANGE RATIO AND DETERMINATION CRITERIA

4.1 Merger of SMILES Shares by GLA

SMILES shareholders may, at their sole discretion, elect the Optional Exchange Ratio, within the period and in accordance with the procedure to be timely informed through a Notice to Shareholders ("Optional Exchange Ratio Period"). SMILES shareholders that do not elect the Optional Exchange Ratio will automatically migrate in accordance with the Base Exchange Ratio in relation to the totality of their shares. The migration based on the Optional Exchange Ratio, as the case may be, may be applied to all or some of the shares held by investors, with the investor indicating the number of shares to be used on said option.

Base Exchange Ratio: for each common share issued by SMILES, four common shares and one GLA Redeemable Class B Preferred Share will be granted; or

Optional Exchange Ratio: for each common share issued by SMILES, one common share and one GLA Redeemable Class C Preferred Share will be granted.

4.2. Merger of GLA Shares by GOL

(i) For each common share issued by GLA, 0.1650 GOL preferred share will be granted; (ii) for each GLA Redeemable Class B Preferred Share, one GOL Redeemable Class B Preferred Share will be granted; and (iii) for each GLA Redeemable Class C Preferred Share, one GOL Redeemable Class C Preferred Share will be granted.

Any fractions of shares issued by GOL under the Merger of GLA Shares will be grouped in whole numbers to be subsequently sold in the spot market managed by B3 S.A. – Brasil, Bolsa e Balcão ("B3"), after the consummation of the Reorganization, in accordance with the notice to shareholders to be timely disclosed. The amounts received in this sale will be made available to the former SMILES shareholders that held the relevant fractions, net of fees and taxes, when applicable, in proportion to the interest they held in each share sold.

4.3. Redemption of Preferred Shares

Upon approval of the Reorganization, the redemptions of GLA Redeemable Preferred Shares and GOL Redeemable Preferred Shares will occur on the same day, immediately and subsequently.

The Withholding Income Tax ("IRRF") levied on the capital gain earned by SMILES shareholders who are residents or domiciled abroad ("Non Resident Shareholders of SMILES"), will be deducted from the proceeds from the redemption of GLA Redeemable Preferred Shares, as a result of the Merger of SMILES Shares by GLA, as described in item 9 below. The remaining amount, after said deduction, will go to GOL, which will be the sole shareholder of GLA.

Proceeds from the redemption of GOL Redeemable Preferred Shares will go to shareholders that then hold shares as a result of the implementation of the procedures described above. In the case of Non-Resident Shareholders of SMILES, proceeds from the redemption of GOL Redeemable Preferred Shares will be net of the IRRF levied on the capital gain earned by them in the previous step (as a result of the Merger of SMILES Shares by GLA), as described in item 9 below.

The redemption of: (i) GLA Redeemable Class B Preferred Shares will occur at R$4.46 per redeemed GLA Redeemable Class B Preferred Share; and (ii) GLA Redeemable Class C Preferred Shares will occur at R$17.86 per redeemed GLA Redeemable Class C Preferred Share.

The redemption of: (i) GOL Redeemable Class B Preferred Shares will occur at R$4.46 per redeemed GOL Redeemable Class B Preferred Share; and (ii) GOL Redeemable Class C Preferred Shares will occur at R$17.86 per redeemed GOL Redeemable Class C Preferred Share.

5. CRITERIA FOR DETERMINATION OF THE EXCHANGE RATIO

The exchange ratio above was submitted by the management of GOL for approval of the shareholders of the companies.

6. SUBMISSION OF THE MERGER FOR APPROVAL OF BRAZILIAN OR FOREIGN AUTHORITIES

The Merger is not subject to the approval of Brazilian or foreign authorities.

7. EXCHANGE RATIO CALCULATED PURSUANT TO ARTICLE 264 OF LAW NO. 6,404/76

In compliance with Article 264 of the Brazilian Corporate Law:

(i) Apsis Consultoria e Avaliações Ltda. ("Apsis") was engaged by SMILES to prepare an appraisal report of the shareholders' equities of SMILES and GLA as of September 30, 2020, both adjusted to market prices and by the same criteria. In view of the GLA's negative shareholders' equity amount assessed at market prices, it was not possible to determine an exchange ratio, as described in the referred report; and

(ii) Apsis was engaged by GLA to prepare an appraisal report of the shareholders' equities of GLA and GOL as of September 30, 2020, both adjusted to market prices and by the same criteria. In view of the GLA's and GOL's negative shareholders' equity amounts assessed at market prices, it was not possible to determine an exchange ratio, as described in the referred report.

8. RIGHT TO WITHDRAW AND REIMBURSEMENT AMOUNT

8.1. Right to Withdraw from the Merger of SMILES Shares

Pursuant to Articles 137 and 252, paragraph 2, of the Brazilian Corporate Law, if the Reorganization is completed, the Merger of SMILES Shares by GLA will entitle SMILES and GLA shareholders to withdrawal rights.

As of the date of the GLA's Shareholders' Meeting that will pass a resolution on the Merger of SMILES Shares, GOL will be the sole shareholder of GLA. Accordingly, there will be no dissenting shareholders or withdrawal rights in GLA in this Reorganization step.

Pursuant to Article 264, paragraph 3 of Brazilian Corporate Law, dissenting shareholders may elect: (i) the reimbursement amount set forth in Article 45 of the Brazilian Corporate Law, in accordance with the financial statements of SMILES as of and for the year ended December 31, 2019, approved at the Ordinary Shareholders' Meeting dated July 31, 2020, corresponding to R$9.71 per share, without prejudice to the right to prepare a special balance sheet; or (ii) the amount assessed pursuant to Article 264 of the Brazilian Corporate Law, corresponding to R$19.60. We clarify that the exercise of withdrawal rights will exclusively refer to all shares. Accordingly, dissenting shareholders cannot partially exercise their options.

8.2. Right to Withdraw from the Merger of GLA Shares

Pursuant to Articles 137 and 252, paragraph 2, of the Brazilian Corporate Law, if the Reorganization is completed, the Merger of GLA Shares by GOL will entitle GLA and GOL shareholders to withdrawal rights. Withdrawal rights will be granted to GOL shareholders uninterruptedly, from February 12, 2021 to the Date of Consummation of the Reorganization, that do not vote in favor of the merger of GLA Shares, abstain from voting or do not attend the relevant Extraordinary Shareholders' Meeting, and expressly state their intention to exercise their withdrawal rights within 30 days from the date of publication of the minutes of the Extraordinary Shareholders' Meeting that approves the Merger of GLA Shares.

As of the date of the GLA's Shareholders' Meeting that will pass a resolution on the Merger of GLA Shares, GOL will be the sole shareholder of GLA. Accordingly, there will be no dissenting shareholders or withdrawal rights in GLA in this step of the Reorganization.

In relation to the withdrawal rights of GOL shareholders, considering that GOL's shareholders' equity assessed according to the method set forth in Article 45 of the Brazilian Corporate Law (without prejudice to the preparation of a special balance sheet) and the method set forth in Article 264 of the Brazilian Corporate Law was negative, the reimbursement amount is zero. We clarify that the exercise of withdrawal rights will exclusively refer to all shares. Accordingly, dissenting shareholders cannot partially exercise their options.

9. OTHER MATERIAL INFORMATION

9.1. Corporate Approvals

The Merger of SMILES Shares, Merger of GLA Shares and Redemption will be given effect subject to the following acts, all of which are interdependent and must be coordinated to occur on the same date. The Extraordinary Shareholders' Meetings of GOL and SMILES will be held, on first call, on March 15, 2021, in accordance with the Call Notices disclosed on the date hereof:

(a) the Extraordinary Shareholders' Meeting of SMILES will be held to, in this order, (i) approve the voluntary delisting from the Novo Mercado segment, dismissing the tender offer, pursuant to Article 42 of the Novo Mercado Regulation; (ii) approve the terms and conditions of the Protocol and Justification; (iii) ratify the appointment of Apsis, as the company responsible for the preparation of the appraisal report of the shareholders' equities of SMILES and GLA, for purposes of Article 264 of the Brazilian Corporate Law; (iv) approve the Reorganization, expressly dismissing the installation of an Independent Committee; and (v) authorize the members of management to subscribe for new shares to be issued by GLA and practice other acts required for the Reorganization;

(b) the Extraordinary Shareholders' Meeting of GLA will be held to, in this order, (i) approve the Protocol and Justification; (ii) ratify the appointment of Apsis, as the company responsible for the assessment and determination of the market value of the shares issued by SMILES to be merged by GLA ("Appraisal Report of the SMILES Shares"), as well as the preparation of the appraisal report of the shareholders' equities of GLA and GOL, for purposes of Article 264 of the Brazilian Corporate Law ; (iii) approve the Appraisal Report of the SMILES Shares; (iv) approve the creation of redeemable preferred shares, and the relevant amendment to the Bylaws; (v) approve the Merger of SMILES Shares and the Merger of GLA shares, in accordance with the Protocol and Justification; (vi) authorize, as a result of the Merger of the SMILES Shares, GLA's capital increase, to be subscribed for and paid by the members of management of SMILES, and subsequent amendment to its bylaws (once the final number of shares has been determined, depending on the exchange ratio to be elected by SMILES shareholders, and, therefore, the final number of GLA shares to be issued as a result of the Merger of SMILES Shares), including the authorization of the Board of Directors to determine, at the time of consummation of the Reorganization, the exact number of shares to be issued, as well as the respective financial amount; and (vii) authorize the subscription, by the members of management, of new shares to be issued by GOL; and

(c) the Extraordinary Shareholders' Meeting of GOL will be held to, in this order, (i) approve the Protocol and Justification; (ii) ratify the appointment of Apsis, as the company responsible for the assessment and determination of the economic value of the shares issued by GLA to be merged by GOL ("Appraisal Report of the GLA shares"); (iii) approve the Appraisal Report of the GLA shares; (iv) approve the Reorganization, in accordance with the Protocol and Justification; (v) authorize, as a result of the Merger of the GLA Shares, GOL's capital increase, to be subscribed for and paid by the members of management of GLA, and subsequent amendment to its bylaws (once the final number of shares has been determined, depending on the exchange ratio to be elected by SMILES shareholders, and, therefore, the final number of GOL shares to be issued as a result of the Merger of GLA Shares), including the authorization of the Board of Directors to determine, at the time of consummation of the Reorganization, the exact number of the shares to be issued, as well as the amounts to be allocated to the capital stock and capital reserve; and (vi) approve the creation of redeemable preferred shares issued by GOL, and the relevant amendment to the Bylaws.

As mentioned in the material fact dated January 18, 2021, GOL will not negotiate the operation with the management of Smiles or with the Independent Committee, so that the Reorganization will be subject to approval of its terms and conditions by the majority of the holders of outstanding SMILES shares in accordance with CVM Opinion (Parecer de Orientação) No. 35/2008. GOL also informs that it does not intend to request the trading of its shares in the Novo Mercado segment of the B3 and, accordingly, the Reorganization will also be subject to approval by SMILES's minority shareholders pursuant to the Sole Paragraph of Article 46 of the Novo Mercado Regulation.

Notice to shareholders will be disclosed, in due time, informing the reference date to determine the SMILES shareholders that will receive shares issued by GOL ("Date of Consummation of the Reorganization").

Shareholders should seek the advice of their legal and tax advisors on the legal, foreign exchange and tax implications deriving from the Reorganization Non-Resident SMILES Shareholders will be subject to withholding of the Income Tax charged on the positive difference, as applicable, between the amount attributed to SMILES shares held by them for purposes of the Merger of SMILES Shares by GLA, adjusted by the deductions set forth in item 2.2, and the corresponding cost of acquisition of the shares held by the relevant Non-Resident Shareholder. Income tax will be withheld from the amount to paid upon redemption of the GOL Redeemable Preferred Shares, in accordance with item 4.3.

The rate applicable for the calculation of Income Tax may vary from 15% to 22.5%, depending on the amount of capital gain. Non-Resident SMILES Shareholders in favored tax jurisdictions, as set forth by tax authorities, are subject to a rate of 25%. The Companies will timely disclose a Notice to Shareholders requesting the information required for this withholding.

If, on this occasion, a Non-Resident Shareholder does not inform its average cost of acquisition or does not send the documentation required, at GOL's discretion, to support the informed average cost, GOL will consider that the cost of acquisition of the Non-Resident Shareholder is zero, and the amount attributed to the SMILES shares held by this Non-Resident Shareholder for purposes of the Merger of SMILES Shares by GLA will be fully deemed a capital gain, as permitted by applicable law.

9.2. American Depositary Receipts – ADRs

GOL Preferred Shares issued to SMILES shareholders under the Reorganization cannot be converted into GOL ADRs for a period of (i) 40 days, from the Date of Consummation of the Reorganization, for all shareholders, except shareholders that reside in the United States; and (ii) one year, from the Date of Consummation of the Reorganization, for shareholders that reside in the United States.

9.3. Availability of Documents

The Proposal of the Management of GOL for the Extraordinary Shareholders' Meeting of the company and the appraisal reports prepared in the Reorganization will be available to shareholders of this company, as of the date hereof, at the respective headquarters, Investor Relations website (http://ri.voegol.com.br/), as well as in the websites of the CVM (www.cvm.gov.br) and B3.

Additional disclosures of information to the market will be timely made pursuant to applicable law.

For more information, see https://ir.voegol.com.br/conteudo_en.asp?idioma=1&conta=44&tipo=66904, access to which is restricted to certain investors as specified therein.

This material fact does not constitute an offer to sell, buy or exchange, or a solicitation of an offer to sell, buy or exchange, any security described herein, and no offer, sale, purchase or exchange of any such security will occur in any jurisdiction in which such offer, sale, purchase or exchange would be unlawful without prior registration or exemption pursuant to the applicable securities laws of such jurisdiction. In particular, any offer, sale, purchase or exchange will be made pursuant to registration under the U.S. Securities Act of 1933 ("Securities Act") or pursuant to an exemption from registration or a transaction not subject to the registration requirements of the Securities Act.

Investor Relations

[email protected]

www.voegol.com.br/ir

+55(11) 2128-4700

Media Relations

Becky Nye, Montieth & Company

[email protected]

About GOL Linhas Aéreas Inteligentes S.A.

GOL serves more than 36 million passengers annually. With Brazil's largest network, GOL offers customers more than 750 daily flights to over 100 destinations in Brazil and in South America, the Caribbean and the United States. GOLLOG's cargo transportation and logistics business serves more than 3,400 Brazilian municipalities and more than 200 international destinations in 95 countries. SMILES allows over 16 million registered clients to accumulate miles and redeem tickets to more than 700 destinations worldwide on the GOL partner network. Headquartered in São Paulo, GOL has a team of approximately 14,000 highly skilled aviation professionals and operates a fleet of 128 Boeing 737 aircraft, delivering Brazil's top on-time performance and an industry leading 20-year safety record. GOL has invested billions of Reais in facilities, products and services and technology to enhance the customer experience in the air and on the ground. GOL's shares are traded on the NYSE (GOL) and the B3 (GOLL4). For further information, visit www.voegol.com.br/ir.

Disclaimer

The information contained in this press release has not been subject to any independent audit or review and contains "forward-looking" statements, estimates and projections that relate to future events, which are, by their nature, subject to significant risks and uncertainties. All statements other than statements of historical fact contained in this press release including, without limitation, those regarding GOL's future financial position and results of operations, strategy, plans, objectives, goals and targets, future developments in the markets in which GOL operates or is seeking to operate, and any statements preceded by, followed by or that include the words "believe", "expect", "aim", "intend", "will", "may", "project", "estimate", "anticipate", "predict", "seek", "should" or similar words or expressions, are forward-looking statements. The future events referred to in these forward-looking statements involve known and unknown risks, uncertainties, contingencies and other factors, many of which are beyond GOL's control, that may cause actual results, performance or events to differ materially from those expressed or implied in these statements. These forward-looking statements are based on numerous assumptions regarding GOL's present and future business strategies and the environment in which GOL will operate in the future and are not a guarantee of future performance. Such forward-looking statements speak only as at the date on which they are made. None of GOL or any of its affiliates, officers, directors, employees and agents undertakes any duty or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except to the extent required by law. None of GOL or any of its affiliates, officers, directors, employees, professional advisors and agents make any representation, warranty or prediction that the results anticipated by such forward-looking statements will be achieved, and such forward-looking statements represent, in each case, only one of many possible scenarios and should not be viewed as the most likely or standard scenario. Although GOL believes that the estimates and projections in these forward-looking statements are reasonable, they may prove materially incorrect and actual results may materially differ. As a result, you should not rely on these forward-looking statements.

Non-GAAP Measures

To be consistent with industry practice, GOL discloses so-called non-GAAP financial measures which are not recognized under IFRS or U.S. GAAP, including "Net Debt", "Adjusted Net Debt", "total liquidity" and "EBITDA". The Company's management believes that disclosure of non-GAAP measures provides useful information to investors, financial analysts and the public in their review of its operating performance and their comparison of its operating performance to the operating performance of other companies in the same industry and other industries. However, these non-GAAP items do not have standardized meanings and may not be directly comparable to similarly-titled items adopted by other companies. Potential investors should not rely on information not recognized under IFRS as a substitute for the GAAP measures of earnings or liquidity in making an investment decision.

SOURCE GOL Linhas Aéreas Inteligentes S.A.

Share this article