Canyon Files Definitive Proxy Materials to Elect One Highly Qualified Director Nominee to the Ambac Board of Directors at Upcoming Annual Meeting

Delivers Letter Urging Stockholders to Enhance the Ambac Board by Voting the GOLD Proxy Card to Elect Experienced Stockholder-Nominated Director Candidate -- Frederick Arnold

LOS ANGELES, April 28, 2016 /PRNewswire/ -- Canyon Capital Advisors LLC ("Canyon Capital"), a leading alternative asset manager serving institutional clients worldwide, and manager of funds and accounts that own almost 5% of the outstanding shares of Ambac Financial Group, Inc. (Nasdaq: AMBC) ("Ambac" or the "Company"), announced this week that it has filed definitive proxy materials with the Securities and Exchange Commission in connection with Ambac's upcoming 2016 Annual Meeting of Stockholders, to be held on May 18, 2016, and has delivered a letter to the stockholders of Ambac.

Canyon is urging stockholders to elect Mr. Frederick Arnold, a highly-qualified nominee, to serve on the Company's board of directors at the upcoming 2016 Annual Meeting.

The full text of the letter follows:

April 28, 2016

Dear Fellow Ambac Stockholder:

Canyon Capital Advisors LLC (together with certain of its affiliates, "Canyon") is the investment advisor to funds and accounts that beneficially own over 2.2 million shares, or almost 5%, of the outstanding common stock of Ambac Financial Group, Inc. ("Ambac" or the "Company").

Over the past several months, we have publicly expressed our significant ongoing concerns with the Company's trajectory, and our belief that further change in the boardroom is needed to prevent continuing destruction of stockholder value.

Recently, we filed definitive proxy materials in connection with the Company's 2016 Annual Meeting of Stockholders, scheduled for May 18, 2016, to (1) elect to the Board Mr. Frederick Arnold, a highly qualified and experienced director who is independent of both Canyon and the Company, to replace Jeffrey S. Stein, and (2) disapprove the compensation of the Company's named executive officers. You can find copies of our proxy materials at the following link: http://www.AmbacStockholderRights.com.

The need for a truly independent, stockholder-proposed director to replace Mr. Stein on the Board is clear:

- Mr. Stein has failed to appropriately supervise management and instead has presided over a 30% decline in Ambac's stock price – underperforming peers – since January 1, 2015, when Mr. Stein became Chairman of the Company and Nader Tavakoli took over as interim CEO.

- Despite that underperformance, in January the Board awarded Mr. Tavakoli an outsized pay package allowing him to earn approximately $40 million if he merely restores Ambac's stock price to when he and Mr. Stein obtained their leadership positions.

- Under Mr. Stein's leadership, Ambac's management has demonstrated a pattern of material misdirection and misrepresentation in its public statements, including in defense of its demonstrably poor record.

- In an effort to distract stockholders from its failings and prevent any further change to the Board, management claims that Canyon's effort to replace Mr. Stein will disadvantage stockholders because of Canyon's supposed conflict. DO NOT BE FOOLED:

- This, along with the false accusations of Canyon's supposed "greenmail" attempt, is nothing more than a smokescreen that should not be allowed to obscure the fact that good governance clearly benefits all stakeholders.

- The goal of our proxy challenge has always been to achieve more effective and honest governance of Ambac in order to counter management's lack of candor, competence and integrity.

- Canyon's holdings in 5% of Ambac's equity and our policy claims make us even more invested in Ambac's capital structure. This overall investment gives Canyon enormous incentive to make sure the Company is properly managed and capital is returned intact.

- Our proxy challenge is not about accelerating pay downs to obtain an enhanced rate of return on our policies, as management is attempting to spin.

- The longer our policies are outstanding, the more interest and gross dollars we earn. Therefore, Canyon is advocating a responsible liquidation that avoids further erosion of stockholder equity through interest accrual and instead returns capital to stockholders.

- Moreover, Canyon's fundamental goal – which Messrs. Stein and Tavakoli seem to oppose – is to restore management integrity so that outstanding liabilities are properly addressed and stockholder value is preserved and enhanced.

- Management has failed to work for stockholders to appropriately remediate claims. It did nothing material in that regard in 2015 and should not be allowed to deflect attention from its failings in this critical area.

- If nothing is done, we believe Ambac's current course of action could leave the stock worthless.

- Despite not writing any new business in roughly eight years, Ambac is now telling stockholders that the Company is not in liquidation and that it intends to "eventually" have its wholly-owned operating subsidiary, Ambac Assurance Corporation ("Ambac Assurance"), continue "as a viable and strong company."

- Management recently suggested it wants to risk your money in speculative new schemes, such as home refurbishing.

- After other Ambac stockholders expressed concerns similar to Canyon's about the Company's trajectory, they were successful in getting a single stockholder-chosen nominee on the Board. Canyon is trying to further balance the Board with one more stockholder-proposed director.

- Fred Arnold is simply a better candidate. He has more relevant experience than Mr. Stein and is not burdened by involvement with Ambac's current failed trajectory.

- We are not seeking radical change overnight. Our proposal merely seeks to establish a more balanced Board with less historical allegiance to Ambac's current management and course that can better assess and oversee the Company's near and long-term strategies.

Canyon requests your support in its efforts to provide Ambac with a more balanced Board capable of legitimately assessing the Company's direction and increasing stockholder value.

Please give us your GOLD proxy card voting "FOR" Mr. Arnold and the Company's candidates for election at the Annual Meeting other than Jeffrey S. Stein, and "AGAINST" Ambac's proposal to approve compensation of the Company's named executive officers.

The Board Under Mr. Stein Has Failed To Guide Ambac's Performance and Has Allowed Management to Mislead Ambac's Stockholders

A board of directors is supposed to oversee a company's strategy and its management. The Board under Mr. Stein has failed in both respects, putting its head in the sand as Ambac has spiraled downward and its management has misled stockholders.

Under Mr. Stein's leadership as Ambac's Chairman, the Company's stock price has fallen dramatically. Despite that, the Stein-led Board rewarded interim CEO Tavakoli with a permanent position and lucrative pay package.

Further, as Chairman of the Board, Mr. Stein failed to hold management accountable for its poor performance. He has also stood by while management has made misleading statements to stockholders, including those in defense of the Company's lamentable track record.

Misleading statements by the Company under Mr. Stein's inattentive leadership as Ambac's Chairman include:

- Management's discussion of the quality of Ambac's operating earnings.

- Management's touting its accomplishments in commuting liabilities.

- Management's assertion that Ambac is not in liquidation and can become a going concern in various unrelated businesses.

- Management's representation of the level of stockholder support for Mr. Tavakoli's tenure.

- Management's claim that Canyon's proposal to replace Mr. Arnold with Mr. Stein presents a "conflict of interest" despite Canyon's substantial investments across Ambac's capital structure and significant interest (aligned with all stockholders) in making sure that Ambac obtain ethical, attentive and effective governance.

- Management's charge that Canyon attempted to "greenmail" Ambac, issuing a false press release and proxy materials that so claims, when, in fact, it appears that Ambac was itself seeking to purchase Canyon's securities.

Ambac needs a board that will independently assure its management's integrity and the wisdom of its actions; the Board under Mr. Stein has failed to provide this oversight.

Unlike Mr. Stein, Mr. Arnold will not bury his head in the sand and ignore red flags like these.

Ambac's Poor Performance

When faced with criticism over the Company's performance under current leadership, Ambac tells you how well it has done since emerging from bankruptcy in 2013. That is irrelevant. What matters is what happened since Messrs. Stein and Tavakoli took over.

- Since January 1, 2015, the date on which Mr. Stein became Chairman of the Board and Mr. Tavakoli took over as Ambac's interim President and CEO, Ambac's stock price has dropped by over 30%.

- Ambac says its stock year-to-date is up 15% versus the S&P 500 being up 2%, but its peer (MBIA) is up roughly 24% year-to-date. Moreover, in the last 12 months – a more significant period – Ambac's stock is down over 30%, while peers MBIA and Assured Guaranty are down approximately 12% and 3%, respectively. Their better performance is despite their own exposure in Puerto Rico, which Ambac tries to blame for its woes.

- Ambac tries to fool you by correlating its stock price with the price of Puerto Rico municipal bonds. But it does so based on dollar change in price rather than percentage change in price, which is the appropriate metric. There is virtually no correlation under the appropriate metric.

- Ambac touts superior operating performance relative to its peers by pointing to its higher adjusted book value growth. But that is meaningless because Ambac emerged from bankruptcy with negative book value and a positive stock price, and its peers are returning capital to stockholders while Ambac is not.

Management claims to have achieved $25 of operating earnings per share in 2015. But that is plainly a distortion and the 2015 stock price drop from $24.50 to $14.09 indicates the market agrees.

- Ambac's calculation adds back intangible impairment and amortization, presumably because such expenses are non-cash and non-recurring.

- At the same time, Ambac fails to adjust for the equally non-recurring gains that resulted from changes in future loss assumptions, such as improvement in housing prices or assumptions around likelihood of future commutations.

- Excluding these assumptions, Ambac lost about $1.75 per share in 2015 – which does not include the economic value lost in missed opportunities to commute policies during the volatility in Q3 and Q4.

- Ambac's CFO has acknowledged that earnings have been beneficially impacted by marketplace dynamics having nothing to do with management, such as in 3Q2015 when "the RMBS loss benefit of $179 million . . . was driven by a decrease in interest rates and improved credit profile of our first and second lien exposures."[1]

The Company also touts its success in cutting costs, but the numbers do not lie and Ambac's expenses have actually increased under Mr. Stein and Mr. Tavakoli.

Photo - http://photos.prnewswire.com/prnh/20160428/361413

- Total 4Q2015 operating expenses increased and total 2015 operating expenses increased 1% versus 2014.

- That does not take into account Mr. Tavakoli's compensation, which could be 10% or more of the entire 2016 compensation budget.

- Ambac's expenses grew in 2015 even though its exposures continued to run off primarily due to municipal refinancings. Stockholders need look no further than MBIA to see the disconnect between Ambac's decreasing exposure and increasing expenses.

- Ambac tries to explain MBIA's decrease in operating expenses during 2015 as a one-off occurrence driven almost entirely by the sale of a business. But selling an unprofitable business is a way to cut unnecessary operating expenses, and MBIA managed to reduce its operating expenses even without that sale.

There is also no basis for other accomplishments Ambac's management would like you to believe.

- Mr. Tavakoli has cited the Company's commutation of Ambac's Eurotunnel exposure. In fact, Eurotunnel presented very little risk to Ambac: the issuer made a financial decision to pay the Company up front to terminate coverage rather than continue to pay the associated premiums.[2]

- Mr. Tavakoli also touts the Company's $399 million reduction in National Collegiate Student Loan Trust exposure. But nearly all of the exposure ($382 million worth) was rated B- or better by S&P and was thus low risk to Ambac; the remaining $17 million reduction was the result of natural bond amortization.

- Ambac also recently boasted of $4.4 billion of total student loan commutations since its bankruptcy, but makes clear that only $800 million of that was below investment grade. Even of the $800 million, much of that carried low risk of loss or was done prior to Mr. Tavakoli's tenure as CEO.

— $194 million is attributable to the B- rated bonds that were low risk and included in the $382 million described above.

— $254 million was purchased in 2014 under Mr. Tavakoli's predecessor and was merely unwrapped during his tenure.

— Based on CUSIP numbers, it appears another $100 million or so was commuted well before Mr. Tavakoli became interim CEO.

— $225 million was purchased in February 2016 only after Canyon's urging.

- During the 3Q2015 earnings call with stockholders, Mr. Tavakoli boasted that "working with the [Puerto Rico] HTA we expect that $228.5 million net par . . . are expected to be canceled at no cost to Ambac." In reality, Puerto Rico had repurchased the associated instruments four years earlier.

- As for the Company's $995 million settlement of residential mortgage-backed securities litigation against JP Morgan, based on publicly available information such as court filings and monthly trustee reports it was for only about 59% of the incurred losses, below the levels of recovery achieved on similar claims by several of the Company's peers, including:

— The 2013 judgment in favor of Assured Guaranty against Flagstar for approximately 118% of the incurred losses;[3]

— The 2013 settlement between MBIA and Flagstar for approximately 67% of the incurred losses;[4]

— The 2014 settlement between Syncora and JP Morgan, which appears to be somewhere between 66-86% of the incurred losses.[5]

— While these precedents all have slightly unique characteristics (e.g. component of future losses), the big picture clearly indicates that Ambac's settlement with JP Morgan was nothing remarkable.

Ambac's Leadership is Over-Compensated

There is no legitimate justification for the Board, under Mr. Stein's leadership, to have approved Mr. Tavakoli's extraordinarily high compensation, especially given the Company's poor performance while he was interim CEO.[6]

On his appointment as Ambac's permanent President and CEO in January 2016, the Board awarded Mr. Tavakoli an additional cash bonus for 2015 – a year in which Ambac's stock price declined by 42.9%.

Under the pay packages awarded by the Board, Mr. Tavakoli could earn approximately $40 million (subject to the satisfaction of certain performance goals and further vesting in 2019 and 2020) even if he merely restores Ambac's stock price to the level it was when he became interim CEO.

Ambac's assertions that Mr. Tavakoli could only reach $33 million at maximum levels does not take into account post-grant stock price appreciation. Such appreciation should indeed be treated as compensation, as is reflected by the fact that it would be taxed as ordinary compensation income and would be reported as compensation income for proxy reporting purposes.

Ambac's further assertion that the stock price would need to increase to $50.70 for Mr. Tavakoli to reach maximum compensation appears to be based on pure speculation. Ambac's Compensation Committee has yet to set the goals governing Mr. Tavakoli's future performance-based stock grants or, if those determinations have been made, has yet to disclose them to stockholders publicly.

Although 2016 information is not yet publicly available for the Company as a whole, Mr. Tavakoli's target and maximum compensation in 2016 would equal at least 11% and 18% respectively of the Company's total 2015 compensation expense. These are remarkable numbers.

Mr. Tavakoli's target pay is over 3 times that of his predecessor. And unlike his predecessor, Mr. Tavakoli is not even required to work full time for the Company.

Ambac suggests that a December 2014 communication from Canyon expressing support for Mr. Tavakoli upon his appointment as interim CEO undermines our present concerns with the Company's leadership. That makes no sense.

- Mr. Tavakoli had no track record as CEO at that point.

- Despite his lack of prior experience, we supported giving Mr. Tavakoli a chance.

- He has proven that he is not fit for the job.

As to Mr. Stein and other members of the Board, in spite of the Company's struggles, Ambac paid its full-year Board members on average over $189,000 more than the compensation paid to the 90th percentile of full-year board members at the companies Ambac itself has identified as its peers for compensation purposes ("Ambac's Chosen Peers").

For 2015, the compensation for each full-year member of the Board was $475,004. By comparison, the median compensation for the 126 full-year board members of Ambac's Chosen Peers is approximately $174,500 – over $300,000 less than what each Ambac Board member takes home.

In fact, only one board member in Ambac's Chosen Peers receives more than each of Ambac's board members – the long-term non-executive Chairman of Radian Group Inc., a much larger company than Ambac that still has active business.

Given their extraordinary compensation, when management and the Board advocate to keep the Company going through speculative, non-core business pursuits, ask yourself who those plans are intended to benefit and who is really conflicted.

We Are Trying to Further Improve Ambac's Corporate Governance

Ambac asks you to consider that its slate of nominees has received public backing from other stockholders. But nearly all of the stockholder support to which Ambac refers is from stockholders who are contractually bound to support that slate.

After extensive criticism from Canyon and its announced intent to nominate three independent directors, other stockholders also pressed for changes in the Board. Ultimately, on March 28, 2016, the Company announced agreements to replace two of Ambac's directors with nominees approved by certain stockholders.

- Only one of those two nominees – Ian Haft – was proposed by the stockholders.

- The other was proposed by Ambac management.

As a result, those stockholders are now required to support Ambac's slate. You and Canyon are not.

Our decision to no longer pursue three nominees is not a "failed initial campaign" as Ambac claims. To the contrary, it is an attempt to build constructively on the work our fellow stockholders have done.

We commend them for successfully getting one stockholder-proposed director on the Board, but one is not enough. Replacing Mr. Stein with a truly independent stockholder advocate will be a very significant improvement.

Ambac Needs a More Balanced Board That Will Honestly Consider Change Rather Than Burying Its Head in the Sand

Canyon has been highly critical of Mr. Tavakoli, but we are not asking stockholders to remove him as a director at this point. We recognize the complications of doing that while he continues to serve as President and CEO.

Nor is Canyon looking to transform Ambac overnight.

We want to replace Mr. Stein to achieve a more balanced Board that can more fairly consider a departure from the Company's failed policies and the bona fides of Mr. Tavakoli's leadership.

Of the six directors on the Company's slate:

- Mr. Haft is the only one proposed by current stockholders.

- Three were proposed by existing leadership.

- The remaining two – Mr. Stein and Mr. Tavakoli – joined the Board together on May 1, 2013 and have served in leadership positions throughout the significant decline in Ambac's stock price since the beginning of 2015.

Mr. Stein has presided as Chairman over the Board during the entirety of Mr. Tavakoli's disastrous tenure as President and CEO and the loss of over 30% of Ambac's equity value that stockholders have witnessed in that time.

Ambac notes it has long-term obligations, and attempts to suggest that Canyon is proposing an irresponsible, immediate liquidation. That is a straw man. Our point is simply that Ambac could be doing much more to address its outstanding liabilities than it is doing now.

As Ambac itself acknowledges, there is also a natural check on the rate at which that will be done: the regulator overseeing the Segregated Account of Ambac Assurance Corporation (the "Segregated Account").

Fred Arnold is not going to instantly reverse Ambac's failed course. But he can help work for responsible change over time through building consensus and taking considered actions.

Canyon Is Not "Conflicted"

Ambac wants you to believe that Canyon is "conflicted" because we also own Ambac Assurance policies. Do not be fooled.

Canyon never had any disagreement with Ambac over reducing policy liabilities. Our concern, and the reason for our proxy challenge, has always been Mr. Tavakoli's lack of candor, competence and integrity.

Canyon is one of Ambac's largest stockholders, holding nearly 5% of Ambac's equity. Ambac's response that there are other stockholders with substantial holdings too is totally irrelevant.

Canyon's policy holdings only mean we are even more invested in Ambac, and have that much more stake in its proper management. It is not uncommon for investors to own securities throughout the capital structure of a company.

All stockholders have a strong interest in ensuring Ambac properly manages its liabilities so they do not erode equity value and defer return of capital.

Given that the regulator concluded that policy claims likely will be paid at par plus accrued interest, any expectation that Ambac will be able to buyback or commute the policy claims at a substantial discount would be delusional.

- As noted, Ambac buybacks in 2015 were at prices as high as over 90 cents on the dollar.

Because of Canyon's significant equity position, and the fact that any discount management achieves on policies is not likely to be substantial, the notion that Canyon is actually conflicted in advocating liability management is absurd.

- For example, if all policy claims were paid down at 82 cents on the dollar, based on current prices, Canyon's equity book value would increase by about $30 million.

Equally absurd is the claim that Canyon is launching a proxy contest to improve the rate of return on claims that, based on expected future losses and recoveries, will achieve par anyway according to the regulator with responsibility for their payment.

A more appropriate way to understand Canyon's stock and debt investments in Ambac is to express them as a percentage of the company's reserves.

- On that basis, Canyon's holdings on the debt side total about 5%, which is the same as its percentage of holdings on the equity side.

- That means dollar for dollar any percentage reduction of Ambac's obligation on the debt side translates into the same percentage gain for Canyon on the equity side.

Although Ambac continually refers to a long-term plan for asset-liability management, it has never clearly articulated what that plan is or any plan for returning capital to stockholders.

- Instead, management appears to be maneuvering to render the policy claims as permanent capital to ensconce its position.

- This "strategy" of holding policy claims indefinitely with the hope of one day being able to resolve them cheaply is an ill-fated fantasy that hurts all stockholders as policy claims continue to accrue and compound interest under the rehabilitation plan.

The real conflict is between stockholders and entrenched management: Ambac's management and the Board have a clear conflict in that as policies continue to run-off – which should be substantial by the end of 2017 – so does their exorbitantly-compensated time at the helm.

The recent agitation by other stockholders that resulted in the appointment of two new Board members reflects that other stockholders, not just Canyon, are concerned.

Management's Lack of Candor

Mr. Tavakoli's tenure has been marked by one unsubstantiated assertion after another of which Mr. Stein was fully aware but did nothing to prevent or correct.

Public – During an interview aired on CNBC on January 24, 2016, Mr. Tavakoli said "we're not aware of any shareholders calling for my ouster."[7]

- Yet Ambac's own proxy states that on December 17, 2015, Canyon "sent a letter to Ambac's Board, in which Canyon, among other things, questioned Mr. Tavakoli's leadership and qualifications to be CEO, recommended that the Board engage with its largest shareholders, including Canyon, regarding potential candidates for the permanent CEO position."

- Similarly, in a letter dated January 7, 2016 to Ambac's Board, Canyon said that the appointment of Mr. Tavakoli as the Company's permanent CEO "flies in the face of our concerns and the market's verdict on his tenure."

Private – In a March 14, 2016 letter to Canyon, Ambac denied that an investor who called in to Ambac's 3Q2015 earnings call to express support for Mr. Tavakoli headed a company at the time a fund managed by Mr. Tavakoli had been a large stockholder.

- That assertion was manifestly false based on Form 13Fs that had been filed – and signed – by Mr. Tavakoli disclosing that his fund had invested in the company for at least nine quarters, at one point holding some 4.5% of its stock.

Manufactured – In an April 11, 2016 press release, Ambac suggested that Canyon had attempted to "greenmail" the Company because a broker purportedly offered to sell Canyon's publicly disclosed securities to Ambac.

- Canyon never directed or authorized anyone to approach Ambac with a proposal, much less at the 17% premium that Ambac claims.

- As Ambac's own press release notes, Canyon's CUSIPs are public and any broker could reference them.

- In fact, a broker approached Canyon indicating that Ambac was interested in buying back all of Canyon's positions. Canyon refused to engage.

- Like management's "conflict" claim against Canyon, the "greenmail" claim is entirely manufactured. Both are nothing more than an attempt to undermine our effort to restore competence and integrity to Ambac.

Ambac IS in Liquidation and Needs to Do More to Return Capital to Stockholders

Unbelievably, in its own letter to stockholders and in a slide deck, Ambac is now denying that it is in liquidation. Instead, it is telling stockholders that it intends "eventually" to have Ambac Assurance continue "as a viable and strong Company." That is insane.

- Ambac has not written any new business in eight years and is highly limited in what it can do.

- Ambac Assurance was ordered by the Office of the Commissioner of the Insurance of the State of Wisconsin ("OCI") under the Wisconsin Insurers Rehabilitation and Liquidation Act to stop writing insurance well before its rehabilitation proceedings began.

Ambac also has made comments over the last several months about starting amorphous, speculative new businesses having nothing to do with its core insurance operations:

- Home Repair

"This October we introduced a pilot program to invest in residential real estate owned properties within Ambac insured transactions. The main component of the value creation of this project will be the result of making repairs to the REO properties in order to bring them up to neighborhood standards."[8]

- Asset Management

"[W]e're giving substantial thought to deploying our capital strategically in asset management businesses."[9]

Who is Ambac kidding? Ambac is playing with your money, and its CEO and Board are drawing down exorbitant compensation while it does so.

Ambac's own management and auditors concluded that there is "substantial doubt about Ambac's ability to continue as a going concern."[10] Management should wind Ambac down, return your money, and move on.

Ambac's failure to address its outstanding liabilities is hurting equity holders

- Until those liabilities are addressed, management cannot return capital to Ambac's stockholders.

- Based on expected future losses and recoveries, OCI concluded that policies in the Segregated Account ultimately will be paid at par plus accrued interest.

- While they remain unpaid, they are accruing interest at a rate of 5.1%. That erodes equity value every day.

- Current claims held by third parties generate $4 per share annually in interest expense.

Ambac says its long-term yield on investible assets in 3Q2015 was 5.93%.[11] We think that is overstated:

- A substantial portion is due to the expected return on Ambac's own repurchased policies.

- Ambac still carries the liabilities associated with those policies, and will be paying itself for any gains supposedly "earned".

- The rate of return Ambac points to does not account for the lower return on short-term investments.

Excluding the notional yield on Ambac's own policies and including short-term investments, Ambac's investment portfolio returned only 2.78% in Q32015, less than half of the 5.93% claimed by Ambac.

- That is also well below the 5.1% interest accruing on the unpaid policy claims, which are carried on Ambac's balance sheet below face value, such that the GAAP interest cost on those liabilities is in fact higher than 5.1%.

- The rate of return would be lower still if cash were included, and it may be even lower going forward due to the recent buildup of cash.

Ambac's Efforts to Address its Liabilities Have Been Woefully Inadequate

We believe Ambac is holding over $2 billion of excess capital, which grows monthly as insured bond exposure rolls off and non-cash assets are realized.

- Ambac does not dispute that it has excess capital.

- Ambac disputes the over $2 billion calculation, saying only that calculating excess capital requires the use of assumptions and subjective judgment.

- In fact, the calculation applies the same metrics used by OCI in its 2014 annual report.[12]

Ambac has shown no urgency in deploying its excess capital. Management has touted its $635 million of insured securities buybacks in 2015, but its actions have been reactive and subscale.

In fact, Ambac failed to engage in any material value-creating commutations in 2015. Very little risky exposure was commuted.

Ambac paid up to 91+ cents on the dollar for these claims, and could have paid less had it bought at a more opportunistic time.

Due to natural run-off of insured exposures and improvement in credit over time, surplus notes have continued to increase in price and will continue to appreciate as credit heals.

- Mr. Tavakoli failed to take advantage of the volatility in pricing, and even conceded that Ambac suffered from "inactivity in the third quarter" of 2015.[13]

Photo - http://photos.prnewswire.com/prnh/20160428/361414

Under Messrs. Tavakoli's and Stein's leadership, Ambac did not begin commuting risky loan exposures until February 2016, following Canyon's continued urging and threat of a proxy contest.

In July 2015, Ambac proposed a transaction to exchange outstanding policy debt obligations that would have been a lose/lose for stockholders and policy claimholders alike.

- Current claims would have received a 25% cash pay down and a 75% exchange into a new junior security issued at a 5% discount to par with a 7% coupon.

- Stockholders would have paid interest at a higher rate than even the current 5.1%.

- Segregated Account policies would have received 100% of future claims, thereby reducing incentive and ability to commute potentially over $2 billion of future claims.

- Management effectively would have trapped capital to invest in its amorphous initiatives and extend their jobs.

- Concerned that Mr. Tavakoli lacked a basic understanding of Ambac, Canyon so informed the Board. Now management wants to deflect those concerns by manufacturing a claim that Canyon is "conflicted."

Strategies for deploying excess capital should include:

- Commutation of current and future large loss exposures, such as

— Student Loans (NCSLT 2007s) in the Segregated Account;

— Ultimate pay RMBS in the Segregated Account;

— Local Insight Media in the General Account;

— Puerto Rico in the General Account; and

— Ballantyne in Ambac UK.

- Claim buybacks in the open market or through public tender.

- If the Company cannot buyback or tender for claims at a discount, it should pay the claims down.

In addition to liability management, the Company's strategy should include:

- Expense savings through operational improvement, which we believe could save stockholders around $1 per share, annually.

- Value maximization of existing assets, including litigation recoveries, on both a present value and nominal basis.

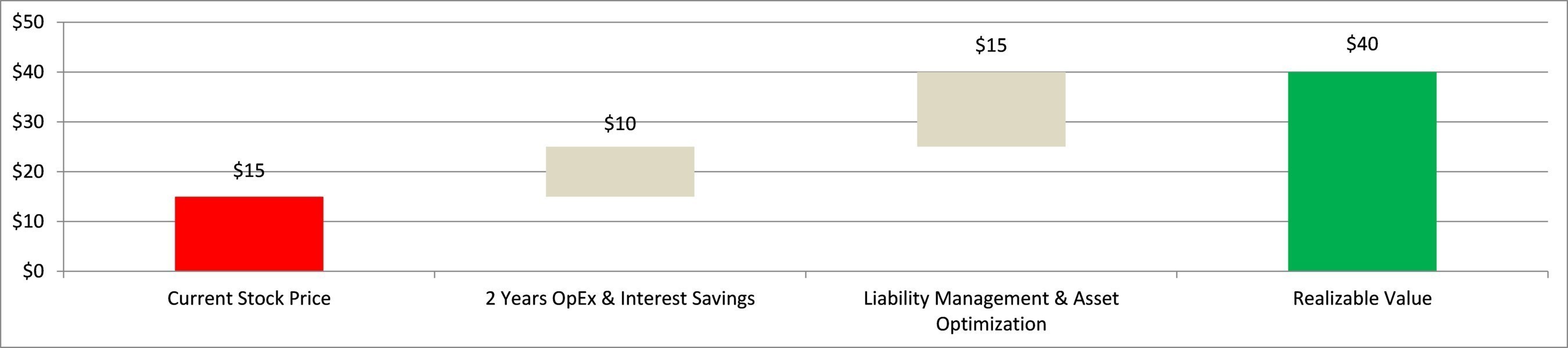

We believe these strategies can return potentially $10 to $20 more per share, and that Ambac's realizable value if properly managed can reach as much as $40 per share, with initial significant dividends to stockholders around the end of 2017:

Photo - http://photos.prnewswire.com/prnh/20160428/361415

Under current management's lack of a clear plan, the unnecessary expenses and interest accruals, along with lack of appropriate liability management, could leave the equity value of Ambac's insurance company worthless.

Mr. Arnold is More Qualified Than Mr. Stein to Help Restore Managerial Accountability to Stockholders

Mr. Arnold has significantly more managerial experience than Mr. Stein in guiding companies through restructurings and dealing with the structured products like Ambac's. We believe he would be a much more vigilant and effective fiduciary for Ambac stockholders.

- Mr. Arnold is Chief Financial Officer and a member of the Executive Committee of Convergex Group, LLC, an agency-focused global brokerage and trading related services provider.

— He oversees Convergex's global financial operations and is responsible for providing organizational guidance and governance.

- Since 2012, he has served as a member of the post-emergence board of directors of Lehman Brothers Holdings, Inc.

- Mr. Arnold also previously served in other senior executive positions, including as Executive Vice President, Chief Financial Officer and a member of the Executive Committee of Capmark Financial Group, Inc.

— He was hired at Capmark to play an integral leadership role in guiding the company through its reorganization and emergence from bankruptcy.

- Before that, Mr. Arnold served as Executive Vice President of Finance for Masonite Corporation, a manufacturing company.

- Mr. Arnold also has significant board-level experience across various types of structured products, including as a director of Corporate Capital Trust, Inc. (since 2011), Corporate Capital Trust II (since 2015), and CIFC Corp. (from 2011 to 2014).

Mr. Stein is an investment professional with no operational experience who never previously held a leadership position with a financial institution.

But Mr. Stein has done this:

- Strongly supported Mr. Tavakoli, whom he calls "an exemplary leader" and whose failed policies he describes as "numerous achievements."[14]

- Presided over the Board during the significant decline in Ambac's stock since early 2015.

- Presided over the Board's year-long purported search for a permanent CEO that resulted in the appointment of Mr. Tavakoli to his current permanent position and its granting him an exorbitant compensation package.

Ambac needs – and stockholders deserve – a Board comprised of directors like Mr. Arnold who are not entrenched, are experienced and are willing to ask tough questions.

Protect and Enhance Your Investment – Vote on Canyon's GOLD Proxy Card

If you agree that stockholders would benefit from a Board better able to fairly and legitimately assess and oversee the Company's direction and managerial leadership, then please vote today "FOR" Fredrick Arnold and the Company's candidates for election at the Annual Meeting other than Jeffrey S. Stein, and "AGAINST" Ambac's proposal to approve compensation of the Company's named executive officers.

Thank you for your support.

Sincerely,

Canyon Capital Advisors LLC

For questions or assistance in voting your shares, please contact:

OKAPI PARTNERS LLC

1212 Avenue of the Americas, 24th Floor

New York, NY 10036

(212) 297‐0720

Stockholders Call Toll‐Free at: (877) 285-5990

E-mail: [email protected]

IF YOU HAVE ALREADY VOTED USING THE COMPANY'S WHITE PROXY CARD, WE URGE YOU TO REVOKE IT. You can revoke it by signing, dating and returning the GOLD proxy card (the latest dated proxy is the only one that counts) or delivering a written notice of revocation or a later dated proxy for the Annual Meeting to Canyon, c/o Okapi Partners LLC, 1212 Avenue of the Americas, 24th Floor, New York, New York 10036 or to the corporate secretary of the Company.

About Canyon Capital Advisors LLC

Canyon Capital Advisors LLC is a leading alternative asset manager serving institutional clients worldwide. The firm seeks to achieve superior, risk-adjusted returns in excess of the debt and equity market indices with lower volatility. Canyon Capital and its affiliates currently manage investment funds and separate accounts amounting to over $20 billion in assets with a staff of over 200, including more than 100 investment professionals. The firm was founded in 1990 and is headquartered in Los Angeles, with offices in London, New York, Shanghai and Tokyo. Canyon Capital has been an SEC registered investment advisor since 1994.

Media Contact

Mike Geller / Nadia Damouni

Edelman

212-729-2163 / 917-344-4771

[email protected] / [email protected]

Investor Contact

Bruce Goldfarb / Pat McHugh / Tony Vecchio

Okapi Partners

212-297-0720

[email protected] / [email protected] / [email protected]

CANYON CAPITAL ADVISORS LLC, THE CANYON VALUE REALIZATION MASTER FUND, L.P., MITCHELL R. JULIS AND JOSHUA S. FRIEDMAN (COLLECTIVELY, "CANYON") AND FREDERICK ARNOLD (COLLECTIVELY WITH CANYON, THE "PARTICIPANTS") HAVE FILED A DEFINITIVE PROXY STATEMENT WITH THE SECURITIES AND EXCHANGE COMMISSION (THE "SEC"), ALONG WITH AN ACCOMPANYING GOLD PROXY CARD TO BE USED IN CONNECTION WITH THE PARTICIPANTS' SOLICITATION OF PROXIES FROM THE STOCKHOLDERS OF AMBAC FINANCIAL GROUP, INC. (THE "COMPANY") FOR USE AT THE COMPANY'S 2016 ANNUAL MEETING OF STOCKHOLDERS (THE "PROXY SOLICITATION"). ALL STOCKHOLDERS OF THE COMPANY ARE ADVISED TO READ THE FOREGOING PROXY MATERIALS BECAUSE THEY CONTAIN IMPORTANT INFORMATION, INCLUDING ADDITIONAL INFORMATION RELATED TO THE PARTICIPANTS. THE DEFINITIVE PROXY STATEMENT AND AN ACCOMPANYING PROXY CARD WILL BE FURNISHED TO SOME OR ALL OF THE COMPANY'S STOCKHOLDERS AND ARE, ALONG WITH OTHER RELEVANT DOCUMENTS, AVAILABLE AT NO CHARGE ON THE SEC'S WEBSITE AT HTTP://WWW.SEC.GOV/, FROM CANYON'S PROXY SOLICITOR, OKAPI PARTNERS, AND AT HTTP://WWW.AMBACSTOCKHOLDERRIGHTS.COM.

INFORMATION ABOUT THE PARTICIPANTS AND A DESCRIPTION OF THEIR DIRECT OR INDIRECT INTERESTS BY SECURITY HOLDINGS ARE CONTAINED IN THE DEFINITIVE PROXY STATEMENT ON SCHEDULE 14A FILED BY CANYON WITH THE SEC ON APRIL 25, 2016. THIS DOCUMENT CAN BE OBTAINED FREE OF CHARGE FROM THE SOURCES INDICATED ABOVE.

[1] Ambac Earnings Call Transcript, 3Q2015.

[2] Eurotunnel press release, dated Dec. 28, 2015 (disclosing that the issuer "sought the removal of Ambac and FGIC as guarantors…[which was] rendered possible by the high degree of predictability of the Group's financial results").

[3] Amended Complaint filed Aug. 19, 2011 and Satisfaction of Judgment filed June 25, 2013, Case No. 11-2375 (SDNY).

[4] Complaint filed Jan. 11, 2013 Case No. 13-0262 (SDNY), Flagstar press release, dated May 2, 2013.

[5] Complaints in Case Nos. No. 09-cv-3106, 651566/2011 (NY Sup. Ct.); 650420/2012 (NY Sup. Ct.); 653519/2012 (NY Sup. Ct.).

[6] Executive compensation and board compensation information is based on the latest statement disclosure as of April 22, 2016, which involved 2015 data for all relevant companies other than four (for which 2014 data is being used).

[7] http://www.cnbc.com/2016/01/14/ambac-ceo-fires-back-over-puerto-rico-strain.html

[8] Ambac Earnings Call Transcript, 3Q2015.

[9] Ambac Earnings Call Transcript, 3Q2015.

[10] Ambac 2015 Form 10-K, filed Feb. 29, 2016, at 67, 74.

[11] Ambac 3Q2015 Operating Supplement at 13, table titled "Income Analysis by Type of Security".

[12] CarVal Affidavit at 9, Feb. 11, 2016, Case No. 10-CV-1576 (Cir. Ct. Dane Cnty. Wis.)

[13] Ambac 4Q2015 Earnings Press Release, dated Feb. 18, 2016.

[14] Ambac Press Release, dated Mar. 9, 2016; Ambac Press Release, dated Mar. 31, 2016.

SOURCE Canyon Capital Advisors LLC

Share this article